Spring Brings Cautious Optimism to U.S. Housing Market

The 2023 outlook we published in January, Staying in Place The Post Pandemic Housing Market anticipated a challenged but resilient U.S. market generally trading sideways this year amid reduced activity and low inventory. Our expectation has been largely realized so far, with national home prices down only 3% from the peak in June 2022, according to CoreLogic Case-Shiller, and recent data have been encouraging.

Demand is down due to the shock in affordability after the sharp rise in mortgage rates in the past year. However, supply is also down as potential sellers, many of whom benefit from existing mortgages at historically low rates, are incentivized to stay put. This is occurring amid a severe housing shortage in much of the country that is likely to support prices.

Challenges remain. National affordability remains at its lowest level since the 1990s. There is potential for more significant price corrections in areas where affordability is most stretched and gains during COVID-19 were most extreme, such as parts of the West Coast and Mountain regions.

Yet an upside surprise for prices – while still not our base case – seems more plausible than it did a few months ago, given the ongoing inventory constraints and the relative pickup in activity, and despite the higher rates. Even after rising significantly, mortgage rates remain in line with historical levels, and a shallow recession could improve affordability if it’s accompanied by lower rates. From an investment standpoint, we believe senior mortgage-backed securities remain broadly attractive.

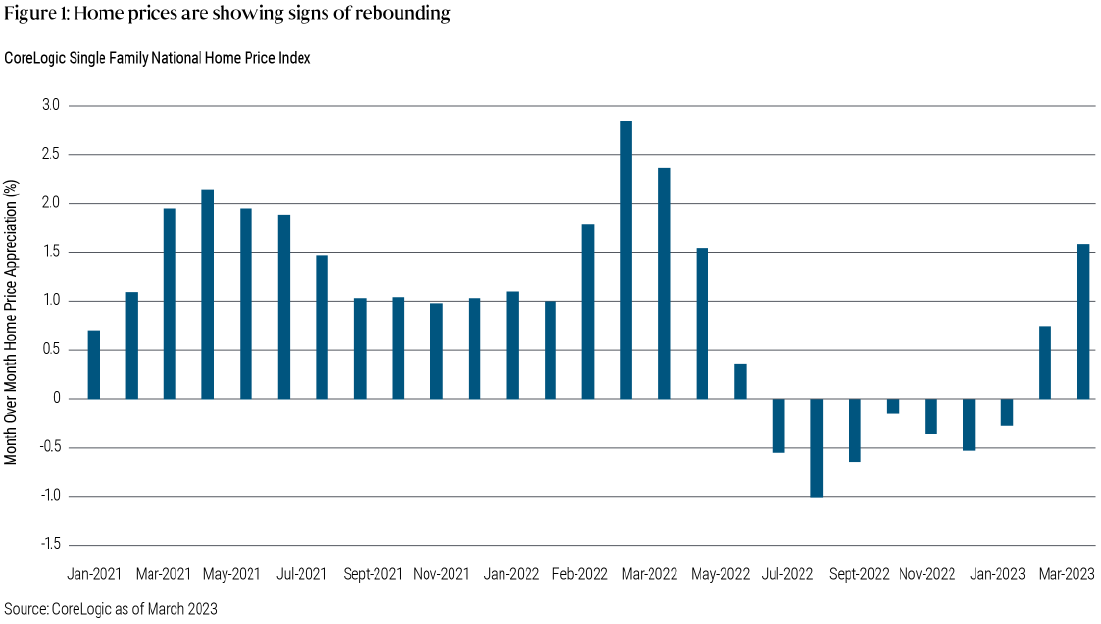

Inventories remain low and activity is perking up

Housing is a highly seasonal market, making spring dynamics particularly important. In March, the inventory of existing homes for sale remained low at 870,000, according to the National Association of Realtors. With home sales increasing to a seasonally adjusted annual rate of 4.4 million, from a low of 4 million in December, the number of months of inventory has dropped back below three, a level that has historically signaled home price increases ahead.

This trend aligns with other data showing improvement since December, when mortgage rates rose above 7%. New and pending home sales have also started to improve, albeit from very low levels. Home prices, as measured by CoreLogic national indices and the FHFA index, have also begun to rise again (see Figure 1). While we caution against reading too much into only a few months of data, the overall trajectory has been improving from the depressed levels of last fall.

Forward-looking activity based on listing data has risen from lows last October. Homebuilders are also reporting pickups in orders. Overall, the supply-demand picture shows about a 30% lower supply from existing home inventory (versus 2018-2019 levels) and lower rental listings while household formation remains normal. In an ordinary environment, such a combination would be a strong positive for the housing market. Further, new home sales (see Figure 2) show the willingness and ability to buy a home remain strong.

Addressing the affordability crisis

This more positive data could appear surprising as mortgage rates are still high compared with last year, with the average national 30-year mortgage rate at 6.88% as of 2 May 2023, according to Bankrate. However, on a historical basis, mortgage rates around 6% are commonplace and are much less of an anomaly than rates in the 2%-3% range.

Affordability has always varied greatly across the different regions of the U.S. For example, Californians have historically paid higher housing costs as a percentage of incomes compared with the rest of the nation. Since affordability in most parts of the country is still better than pre-COVID California levels, this suggests that the percentage of income homeowners can allocate to housing costs has not yet reached its possible maximum in many areas.

In this framework, where affordability effectively serves as a cap on local home values, prices in regions like California and the Pacific Northwest could continue to adjust to achieve more sustainable levels. Meanwhile, in other parts of the country, homeowners may adapt to the decreased affordability by dedicating a larger portion of their income to housing costs.

In addition, while affordability is typically estimated at the current level of mortgage rates, it is likely that a cohort of prospective homebuyers is considering current rates to be temporary and is willing to take advantage of a softer housing market with the hope of refinancing at a lower rate in the future.

Cautiously optimistic outlook amid uncertain conditions

We believe there is reason to remain cautious about the trajectory of housing prices. Another move higher in interest rates, with mortgage rates rising above 7% again, could quickly dampen the recent uptick in housing activity. And while we don't believe the recent banking crisis will significantly affect credit availability – as most mortgages are now originated by non-banks – we must consider the high likelihood of a recession later this year, which would affect consumer sentiment and the housing market at large.

Nevertheless, in our economists’ base case of a shallow recession with the risk of something deeper (for more detail, see our latest Cyclical Outlook, Fractured Markets, Strong Bonds") the impact on housing should be muted as consumers remain protected by their still-healthy balance sheets. Further, if such a recession is accompanied by lower rates – either by way of U.S. Federal Reserve interest rate cuts or markets pushing bond prices higher – it could even end up being a net positive as it could ease the affordability situation.

In terms of investment implications, we continue to find value in senior debt backed by U.S. residential mortgages, which may continue to benefit from a resilient housing market. A combination of an improving outlook on housing, low starting loan-to-value ratios, and wide spreads make securitized credit backed by residential housing an attractive opportunity, in our view.

Featured Participants

Disclosures

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.