Mid‑Cycle Investing: Time to Get Selective

- The global economy is in a mid-cycle expansion, following peaks in policy support and growth, and what is likely a transitory spike in inflation. We expect global growth to moderate to a still above-trend pace in 2022.

- Growth-oriented assets, such as equities and credit, tend to perform well in a mid-cycle environment, but with significant differentiation. Sector and security selection remain crucial. Within multi-asset portfolios, we generally prefer equities over other risk assets based on relative valuations.

- Looking beyond the business cycle, we also assess the potential impact of longer-term disruptions. Trends toward sustainability and evolutions in technology present investment opportunities as well as risks.

Asset Allocation Outlook

The dramatic and uneven rebound in growth across countries this year is likely to ease to synchronized moderation in 2022, though to a still above-trend pace.

We expect not only a peak in growth, but also in inflation and policy support. The global pandemic also appears to be waning. These four peaks were a focal point of our investment forum in early June, and the takeaways are discussed in detail in our recently published Cyclical Outlook, “Inflation Inflection.”

We believe the global economy, as it moves beyond these peaks, is now in mid-cycle. From an asset allocation perspective, this means growth-oriented assets, such as equities and credit, may still offer relatively attractive returns. But we expect greater dispersion across sectors and regions. Moreover, elevated valuations and lower yields portend lower beta returns. Bottom-up differentiation within asset classes – such as country, sector, and issuer selection – will likely be key to driving returns in the current environment.

The peaks

Thankfully, the worst of the global pandemic appears behind us as vaccines proliferate and many countries approach herd immunity.

Still, a receding pandemic also means receding policy support. Fiscal support naturally tied to calendar dates or unemployment levels is rolling off, with the fiscal impulse set to turn negative, as we have already seen in China. On monetary policy, some central banks have moved toward policy normalization by tapering asset purchases (Bank of Canada, Bank of England) or raising rates (some emerging market (EM) central banks). In the U.S., the Federal Reserve in June indicated its intent to begin discussing tapering asset purchases at upcoming meetings, and its projected path of future policy rate hikes (the “dot plot”) was moved up. We expect major developed market (DM) central banks to begin hiking rates in 2023.

While inflation has surprised higher and sparked some fears, we maintain that the world is witnessing a transitory spike, driven by year-over-year base effects, supply bottlenecks, and temporary shortages, that should also moderate into 2022.

A mid-cycle backdrop

The removal of both fiscal and monetary policy support will serve as a drag on economic growth over the next year, even as the easy gains from reopening are realized. We expect developed market real GDP will grow 6% in 2021 (measured by 4Q over 4Q) and moderate to below 3% in 2022. Slower vaccination rates have delayed the recovery in emerging markets, and we expect EM GDP growth to accelerate up to 5% in 2022 (4Q/4Q), after growing 3.5% in 2021.

Although growth rates are expected to peak this year in DM and moderate from current levels, the absolute level of growth will remain high over the cyclical horizon. Pent-up demand, high levels of consumer saving, and healthy corporate leverage ratios create a runway for private-sector-led growth. This provides an attractive backdrop for growth-oriented assets.

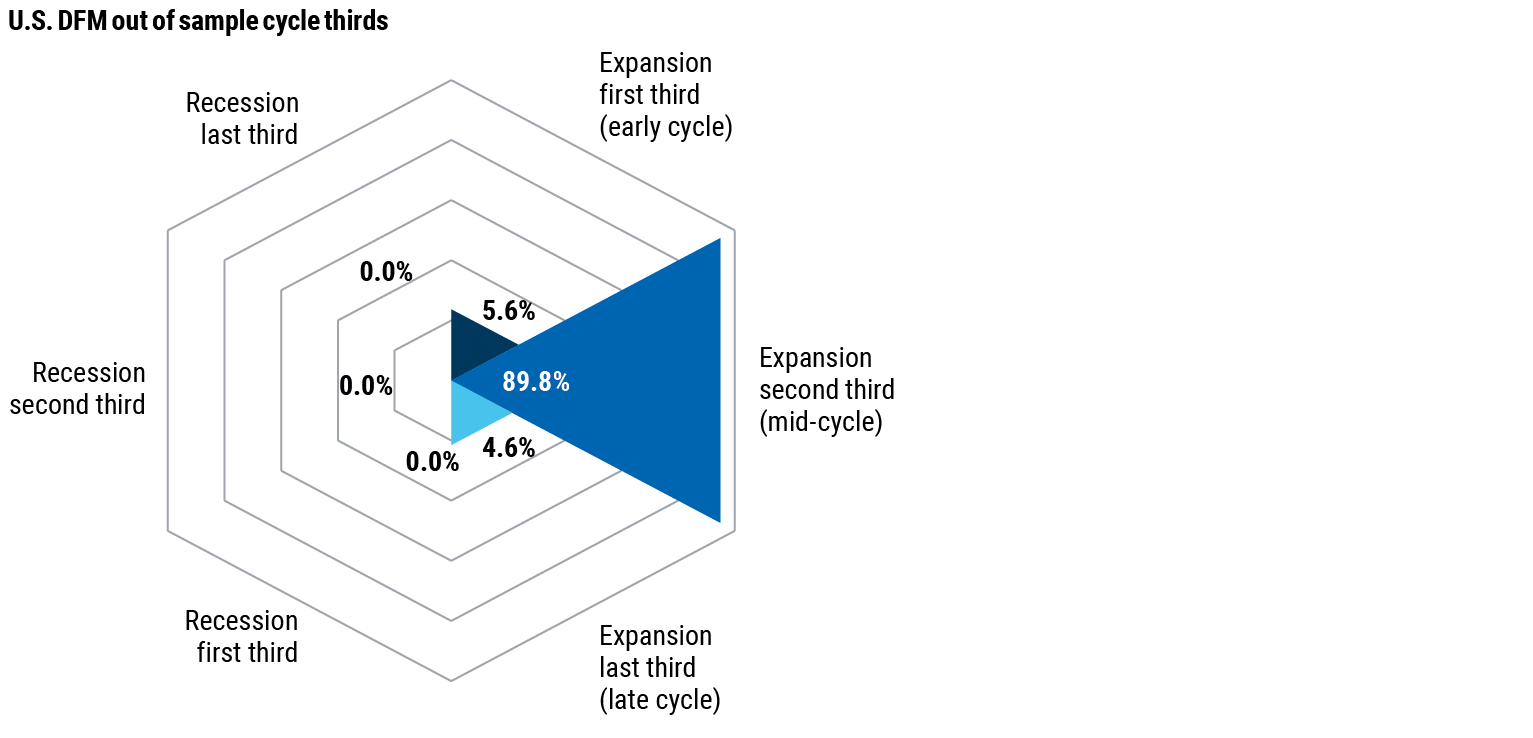

In aggregate, our assessment is that the economy is mid-cycle (see Figure 1), and we believe this is reflected in equity valuations. Historically, these periods have seen strong but differentiated returns in equity markets. Credit also tends to have positive returns in this environment, but often underperforms equities on a risk-adjusted basis. Conversely, the U.S. dollar traditionally has had negative returns in these periods.

Mid-cycle expansions are typically desirable periods to be invested, but with risk premia compressed across markets, investors will have to rely more on sector and security selection to drive returns. This is particularly true in a rapidly changing post-pandemic world where traditional investing patterns may not readily apply, and where uncertainty around potential outcomes is large.

Potential disruptors

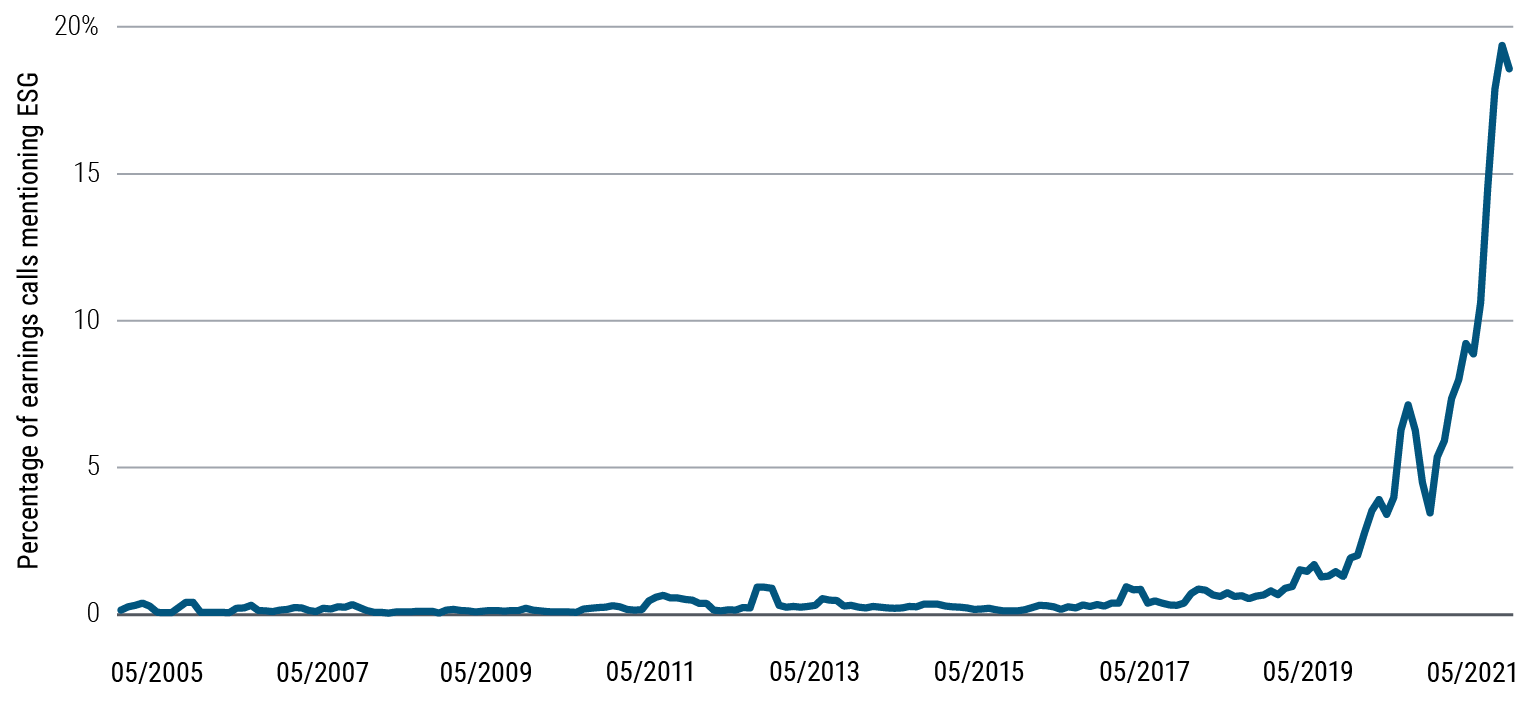

What may be different this time? One trend gaining ground in tandem with the current mid-cycle recovery is ESG investing (environment, social, and governance). Corporate earnings calls, for example, have seen a dramatic increase in mentions of ESG since the onset of the pandemic (see Figure 2). Mapping these ESG influences helps inform asset allocation strategy.

As per the UN, more than 110 countries globally representing over 70% of world GDP have pledged to a net zero carbon future. While this is going to play out over multiple decades, changing investment and consumption should create strong demand for certain goods and materials (for example, renewable energy, semiconductors, and forestry and pulp products). Simultaneously, the net zero trend is likely to leave certain businesses facing risky transitions or long downturns (for example, those companies in the traditional oil and gas sectors that have yet to adjust to the changing energy mix of the future). The move toward a greener future necessitates adoption of new technologies and new energy sources, as well as updated regulations and policies.

Long years of growing inequalities coupled with the pandemic have hopefully awakened a collective social consciousness, which means that previous business practices are increasingly questioned: Zero- hour contracts are being outlawed (the U.K. is one example), we are seeing minimum wages going up (sometimes sharply, and notably among some major employers in the U.S.), and working conditions are being improved in favor of employees (as either mandated by authorities or voluntarily enacted by employers, including in the U.S.). These changes will inevitably have trickle-down effects on smaller businesses.

Also, for the first time ever, there is a genuine concerted dialogue among Organisation for Economic Co-operation and Development (OECD) nations to come up with a global minimum corporate tax rate. The G-7 has proposed a rate of at least 15%. The impacts could be broad, and certain companies could see their taxes go up. Demand for automation and advanced technology (such as artificial intelligence) could be one response, which is a likely long-term positive for industry leaders in these sectors. However, broader redistribution of income could also mean more economy-wide consumption and less propensity to save.

From a governance lens, governments and companies may make increased investments within their borders in order to shorten supply chains and ensure their ability to produce strategic goods like semiconductors, batteries, or medical supplies. In these cases, national or economic security interests may tend to trump economic rationale, and we could therefore see more investment than would otherwise be necessary. Also, a number of industries that suffered during the previous cycle and had to consolidate aggressively are regaining bargaining power over their customers – maritime transport is one example. Indeed, the structures of certain industries are more concentrated now, which seemingly brings better supply discipline, longer-term contracts, and pricing power.

These are some of the factors we include in our top-down asset allocation framework and our bottom-up security selection process in an effort to deliver more robust portfolio outcomes. Within PIMCO’s multi-asset portfolios, this ESG lens has us favoring an overweight in select companies in green sectors (such as renewable energy), digital sectors (such as semiconductors), along with forestry and pulp products, while we remain cautious on fossil fuel industries.

Investment takeaways

With the economic expansion likely at mid-cycle, we generally favor equities and credit, which historically have tended to do well in this environment. In equities, we focus on companies positioned to benefit from secular disruptions in technology, geopolitics, and sustainability. In credit, we are selective, with a focus on housing-related sectors.

Return dispersion across assets is typical during mid-cycle environments, and every cycle is different. Uncertainty surrounding the uneven recovery from a pandemic-driven recession calls for flexibility and a careful eye toward sector and security selection. Our emphasis in multi-asset portfolios is on the bottom-up opportunities within asset classes that can outperform as beneficiaries of the ongoing recovery as well as longer-term disruptions.

Featured Participants

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

Socially responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgment exercised, by PIMCO will reflect the beliefs or values of any one particular investor. Information regarding responsible practices is obtained through voluntary or third-party reporting, which may not be accurate or complete, and PIMCO is dependent on such information to evaluate a company’s commitment to, or implementation of, responsible practices. Socially responsible norms differ by region. There is no assurance that the socially responsible investing strategy and techniques employed will be successful.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

The terms “cheap” and “rich” as used herein generally refer to a security or asset class that is deemed to be substantially under- or overpriced compared to both its historical average as well as to the investment manager’s future expectations. There is no guarantee of future results or that a security’s valuation will ensure a profit or protect against a loss.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2021, PIMCO.