We Believe

- Global output and demand are likely to rebound strongly in 2021, driven by the rollout of vaccines and continued fiscal and monetary policy support. Inflation should creep up only moderately in 2021. Central banks’ policy rates are likely to remain low, and asset purchases will likely continue.

- Key risks to our baseline cyclical outlook include fiscal fatigue (in which governments return to a more cautious stance), a negative credit impulse in China, and pandemic-related economic scarring.

- While equity and credit markets seem to have priced in a return to normality, we see opportunities in non-agency mortgages and other structured products, select corporate credits, and emerging markets. We remain focused on careful portfolio positioning, capital preservation, and liquidity management: This is not a time for excessive optimism.

Economic outlook

We expect the global economy to continue its transition from hurting to healing in 2021 and make good progress on the long climb back to its pre-crisis trend (as we discussed in prior outlooks), especially in the second half of this year. However, while risk markets can continue to perform well in the near term as the dual impact of policy stimulus and vaccine rollout takes hold, much of this is now priced in, and on the path to full recovery investors should beware of obstacles that command careful portfolio construction to weather renewed bouts of volatility in financial markets.

Fiscal fatigue in some advanced economies is one such risk. Another is the likely transition in China from credit easing to tightening in the course of this year. Moreover, economic scarring could impede the return to pre-pandemic activity levels and make the recovery bumpy and uneven across countries and sectors.

Growth bounce

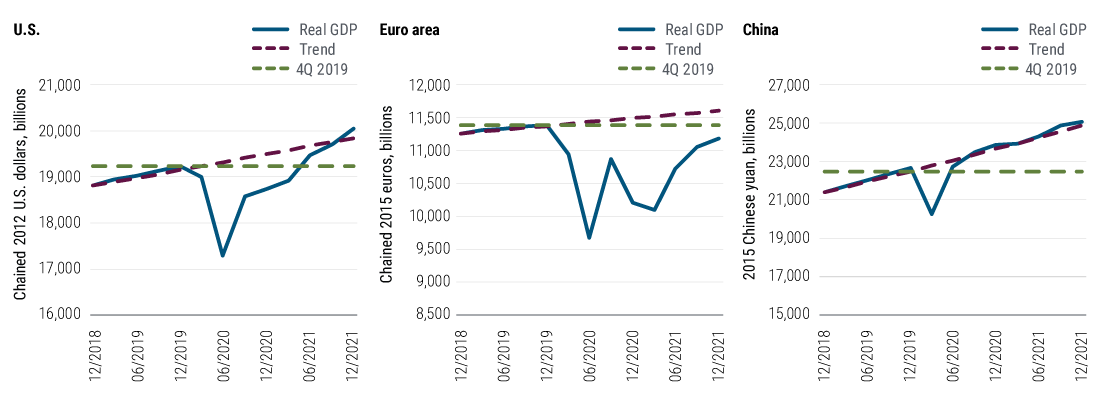

Following an outsized contraction of economic activity in 2020, global output and demand are likely to rebound strongly this year. We expect the current renewed weakness due to lockdowns in major economies to give way to accelerating economic growth from around the second quarter, driven by the broadening rollout of vaccines and continued fiscal and monetary policy support. The sectors most hit by COVID-19-related restrictions – travel, lodging, restaurants, leisure, etc. – should benefit the most. Coming off a low base, world GDP (gross domestic product) growth in 2021 is expected to be the highest in more than a decade. We forecast economic activity in the U.S. to reach pre-recession peak levels during the second half of this year, while Europe, due to its current double-dip, is unlikely to fully make up the output losses until the middle of 2022 despite the sharp growth bounce we expect from the second quarter (see Figure 1). Meanwhile, the Chinese economy, which already operates above pre-crisis levels and has exhibited strong growth momentum into the new year, should record GDP growth above 8% in 2021, after a decidedly subpar 2% or so last year.

Figure 1: Projected path of the level of real GDP in three major economies

Inflation targets remain elusive

Consumer price inflation is likely to creep up only moderately during this year and generally remain below central banks’ targets in all major economies. Even with a sharp growth rebound, output and demand will continue to operate below normal levels for quite some time given the depth of the recession and unemployment, which, while likely to decline, will remain above levels generally associated with full employment. In the U.S., low mortgage rates and downward pressure on rents in the next couple of quarters will weigh on the shelter component of the consumer price index (CPI), which accounts for slightly more than 40% of core CPI. Globally, however, while near- and medium-term inflation pressures are expected to remain low, we reiterate our secular view that the pandemic and related policy responses have increased both longer-term inflation and deflation risks. If monetary and fiscal policies remain expansionary for several years to come even after economies return to full employment, inflation could exceed central banks’ targets eventually. Conversely, deflationary risks could result from a possible return to passive or restrictive fiscal policies or from bursting asset price bubbles and deleveraging of the private sector. As a consequence, we think markets will have to price in higher long-term inflation uncertainty.

Central banks stay the course with bias for further easing

Central banks will remain hostage to inflation running below target and the need to keep borrowing costs low in order to enable ongoing fiscal support for years to come. Thus, policy rates are likely to remain at present levels in the foreseeable future or could even be reduced further in some countries. For example, while not our base case, an excessive appreciation of the euro could induce the European Central Bank (ECB) to further cut its deposit rate, which currently stands at −0.5%.

Moreover, central banks’ asset purchases are likely to continue throughout, and likely well beyond, this year. In the U.S., the Federal Reserve adjusted its guidance in December, stating that it intends to continue with purchases of U.S. Treasuries and agency mortgage-backed securities (MBS) at least at the current pace until “substantial progress” toward its statutory goals of maximum employment and price stability has been made. We see a distinct possibility that the Fed will increase the weighted average maturity of its bond purchases this year if the economy disappoints or if yields rise too fast and too far. In an adverse scenario of renewed economic and financial market turmoil, we would also expect the Fed to restart several of the lending facilities put in place during the 2020 crisis, with equity backing from the Treasury led by incoming secretary Janet Yellen via the Exchange Stabilization Fund or with a new authorization from Congress. Conversely, if the economy rebounds even more strongly than in our base case and inflation surprises on the upside, the Fed may start to gradually taper its purchases already in late 2021 or early 2022.

Meanwhile, the European Central Bank (ECB) recently increased the overall “envelope” for its Pandemic Emergency Purchase Program and is likely to flexibly fill the envelope in the course of this year, aiming to keep euro area bond yields anchored via a form of loose yield curve control. Most other central banks in advanced economies are pursuing similar policies and are likely to stay the course as well. Moreover, further monetary easing appears likely in a number of emerging market economies where real interest rates, while below historical norms in many cases, still have room to decline.

Fiscal policy supportive for now

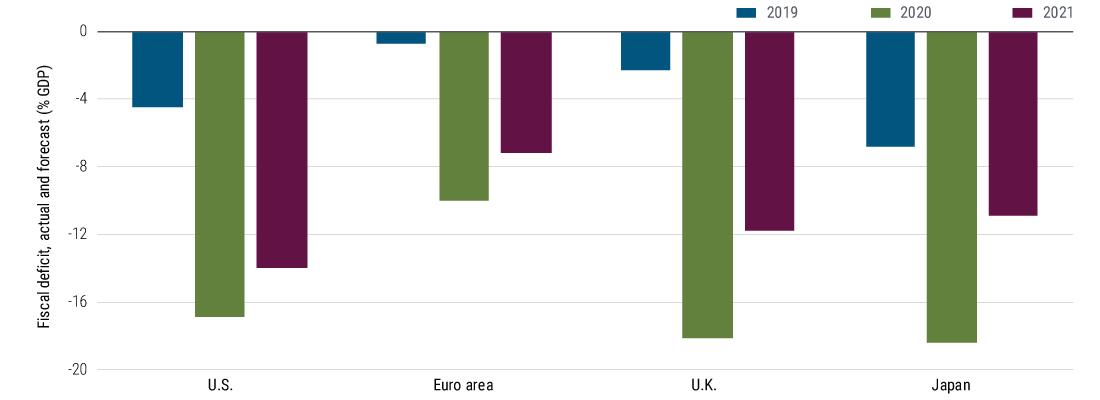

In addition to virus containment through the rollout of vaccines, fiscal policy remains the main swing factor in our cyclical outlook (see more on the downside potential in our Risks section). Aided by monetary policies that keep funding costs low, most governments are likely to keep propping up household incomes via transfers and supporting companies via loan guarantees, subsidies, and tax breaks (see Figure 2). In Europe, the agreement on the European Union (EU) budget in December paved the way for sizeable disbursements of loans and grants from the new EU Next Generation Fund in the course of this year, thus complementing the support coming from national budgets.

Figure 2: Forecast for fiscal deficits in four major economies (as percentage of GDP)

In the U.S., the latest pandemic relief package passed by Congress during the lame-duck period will underpin income and demand in coming months, extending the bridge to economic recovery. Additional significant fiscal support later this year has become likely with the Democrats securing a slim majority (with Vice President-elect Kamala Harris’s vote acting as tiebreaker) in the Senate following the Georgia runoff on January 5. However, given that several new Democratic senators won their seats in traditionally more fiscally conservative states, we do not expect a shift to more radical fiscal policies in the foreseeable future.

Investment conclusions: baseline outlook

As we laid out in the October 2020 Secular Outlook, we expect a fairly range-bound environment for government bond yields over the coming few years. Central banks across the board have signaled that it will be a very long time before we see policy rate tightening, including in the event that our baseline recovery outlook over the next year to 18 months is confirmed. Markets have priced in to a large extent the outlook of recovery but anchored yield curves, with equity markets and credit markets similarly pricing in the return to post-pandemic normality over the cyclical horizon.

We see both upside and downside risks to government bond yields in the near term, reflecting the push and pull between lockdowns and reduced activity and vaccine rollout. In most of our portfolios, we anticipate being fairly neutral on overall duration. U.S. duration continues to offer greater potential capital gains in the event of an economic or financial market downturn – but a less pronounced advantage after the outperformance of U.S. Treasuries over the course of 2020.

While fairly neutral overall on duration, we expect to have curve-steepening positions in our core bond portfolios, given the expectation that while central banks will anchor front ends, over time markets will price greater reflation into the longer ends of curves. We see little inflation upside risk over the cyclical horizon, but greater uncertainty over inflation outcomes over longer time frames, given the extent of monetary and fiscal policy experimentation. We continue to see U.S. Treasury Inflation-Protected Securities (TIPS) offering a reasonably priced hedge against higher inflation over the secular horizon.

Given our baseline outlook and market pricing, we anticipate having overweight spread positions in our portfolios, coming from non-agency mortgages and other structured product positions, carefully selected corporate credit overweights, and hard-currency-denominated emerging market sovereign credit exposures. We will be careful to avoid generic tight corporate credit positions, preferring to rely on the picks of our credit teams and otherwise the liquid credit default swap indices for beta exposure.

We continue to favor agency mortgage-backed securities (MBS), balancing still attractive carry in the lower coupon mortgages and solid Fed support versus valuations that we believe are now fair rather than cheap.

On emerging markets (EM), in addition to EM external positons, we expect to have select EM local positioning where appropriate, with careful scaling given liquidity considerations and a medium-term orientation in these markets.

On currency positioning, we expect to maintain a modest U.S. dollar underweight versus the basket of G-10 currencies and select EM currency exposures in our more globally orientated portfolios. This reflects valuations and the potential for currencies of countries more exposed to the global economic cycle, and hence likely to benefit during the recovery period we envisage, to outperform versus the U.S. dollar.

Risks to the outlook: #1 is fiscal fatigue

Of course, there are risks to our economic outlook, and further investment implications related to those risks.

To begin with, while our base case assumes continued fiscal policy support aided by loose monetary policy, an onset of fiscal fatigue would be a significant risk to the expected economic recovery, particularly in the second half of this year and more so in 2022. In the U.S., while additional fiscal support this year looks likely after the Democrats secured a slim majority in the Senate with the Georgia runoff, later this year the focus may well shift to potential increases in corporate and top personal income taxes to be enacted in 2022.

In Europe, fiscal stimulus is largely baked in the cake for 2021 via already agreed national budgets and the coming disbursements from the EU Next Generation Fund. However, the reality of large deficits could start to affect policymakers’ willingness to stay the course and add additional stimulus if needed. The budget season for the following year traditionally starts after the summer in Europe, and a change in the fiscal policy course for 2022 could thus come into view by the second half of this year. This will be aggravated by the debt brake in the German constitution, which was temporarily waived for 2020 and 2021 but will require budget cuts in 2022 and beyond. Expectations of future fiscal belt-tightening via spending cuts and tax hikes may well start to affect consumer and corporate spending plans in the course of this year.

Risk #2: China refocusing on deleveraging

With China’s economy having rebounded strongly from the COVID-19 recession a year ago and exhibiting strong growth momentum coming into 2021, we expect policymakers to refocus on deleveraging in the course of this year with a view to avoiding bubbles and ensuring long-term growth sustainability. Our China team therefore expects overall credit growth to decelerate this year, resulting in a swing from a recently positive to a negative credit impulse. (Loosely speaking, the credit impulse measures the change in credit growth and typically leads GDP growth.) Calibrating just the right amount of credit easing or tightening in a highly leveraged $14 trillion economy is fraught with difficulties, which implies a real risk of overtightening causing a sharper-than-expected growth slowdown with negative global repercussions in economies and sectors heavily dependent on demand from China.

Risk #3: Economic scarring

The greatest uncertainty in the economic outlook stems from potential scarring effects that could inhibit or even prevent a swift return to pre-pandemic levels of consumer spending as well as corporate investment and hiring decisions. Given the unprecedented nature and size of the COVID-19 shock, it is hard to gauge the behavioral changes of households and firms. While our baseline view assumes that significant pent-up demand will be unleashed this year as the rollout of vaccines allows a rollback of voluntary and government-mandated restrictions on economic activity, there is a significant risk that private households and firms remain more cautious in their spending and investment patterns for longer. Also, labor force participation, which declined in many countries last year, may not recover quickly. Lasting damage to corporate balance sheets and business models could only become apparent during the recovery as government support expires over time.

Investment conclusions: risk factors

While risk markets can continue to perform well over the coming months in response to broadening vaccine rollout and policy stimulus, investors may have become too complacent as reflected by the bullish consensus positioning. As these risk factors underline, we see this as a time for careful portfolio positioning and not for excessive optimism or risk-taking. Given the overall low level of yields, tight spreads, and low volatility, we plan to place significant emphasis on capital preservation and careful liquidity management. We will look to be patient and flexible, to guard against a rise in market volatility, and seek to add alpha in more difficult market conditions. Fiscal fatigue could contribute to a subpar recovery, offsetting other risks to the overall level of global yields. China’s deleveraging underlines the downside risks to overall global growth as well as sector-based risks and risks to individual countries most exposed to China’s cycle. The risk of economic scarring underlines the point that while there are good opportunities in leisure and travel-related sectors, what is needed is carefully managed exposures and not an across-the-board effort to buy securities at low U.S. dollar prices. We believe private credit strategies provide an attractive vehicle for taking long-term positions in the most opportunistic and high risk sectors.

As outlined in the Secular Outlook, in addition to these cyclical sources of risk, a set of secular disruptors leads us to expect that the post-pandemic recovery will not kick-start another decade-long bull market. Rather, once the easy pandemic recovery trades have played themselves out, we expect a difficult market environment. As active managers, we will look to add value with security selection across credit sectors, with a focus on high quality sources of income, and seek to find the best global opportunities.

Download PIMCO's Cyclical Outlook

Download PDFPowered by Ideas, Tested by Decades

About our forums

Honed over nearly 50 years and tested in virtually every market environment, PIMCO’s investment process is anchored by our Secular and Cyclical Economic Forums. Four times a year, our investment professionals from around the world gather to discuss and debate the state of the global markets and economy and identify the trends that we believe will have important investment implications.

At the Secular Forum, held annually, we focus on the outlook for the next three to five years, allowing us to position portfolios to benefit from structural changes and trends in the global economy. Because we believe diverse ideas produce better investment results, we invite distinguished guest speakers – Nobel laureate economists, policymakers, investors, and historians – who bring valuable, multidimensional perspectives to our discussions. We also welcome the active participation of the PIMCO Global Advisory Board, a team of world-renowned experts on economic and political issues.

At the Cyclical Forum, held three times a year, we focus on the outlook for the next six to 12 months, analyzing business cycle dynamics across major developed and emerging market economies with an eye toward identifying potential changes in monetary and fiscal policies, market risk premiums, and relative valuations that drive portfolio positioning.