Looking Beyond the Many Recessions

- We see a sharp contraction in economic activity around the world in the first half of the year as measures to combat the spread of COVID-19 have forced businesses to close and consumers to shelter in place.

- Yet the unprecedented fiscal and monetary policy stimulus enacted to date, along with a gradual easing of quarantine measures, will likely lead to a rebound in activity starting in the second half of this year.

- Still, economic activity may not reach 2019 peak levels for some time, and risks remain tilted to the downside given possible delays in containing the virus and the risk of a second wave of infections.

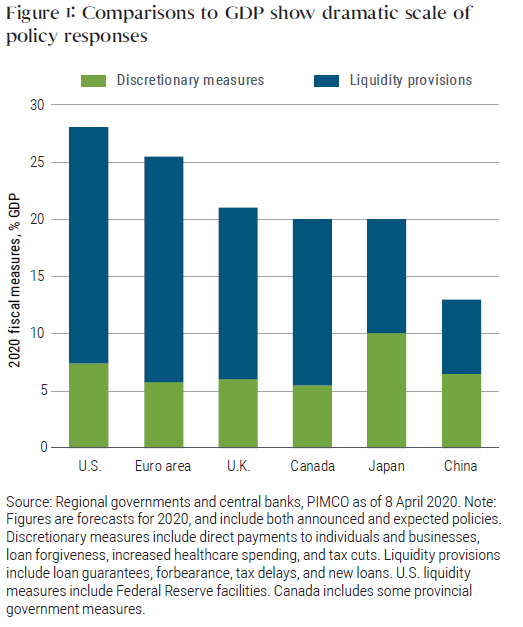

Nations around the world are facing unprecedented challenges in confronting the COVID-19 health crisis. In addition to trying to save as many lives as possible, policymakers are grappling with plummeting business and consumer activity amid near-term fears and longer-term uncertainties, and they are responding with dramatic monetary and fiscal actions to bolster industries, businesses, and individuals (see Figure 1). Results of these extraordinary efforts will vary across regions.

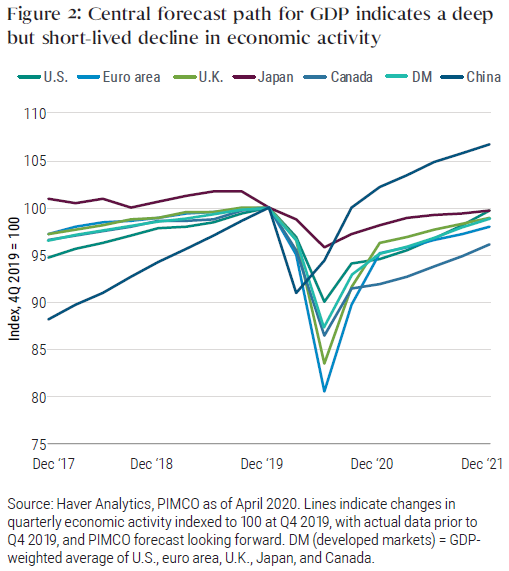

As we discuss in our latest Cyclical Outlook, “From Hurting to Healing” by Joachim Fels and Andrew Balls, we expect the global economy and financial markets to transition from intense near-term pain to gradual healing over the next six to 12 months (see Figure 2). However, there is the risk if not the likelihood of an uneven recovery, with significant setbacks along the way and some permanent damage.

Expanding on those views, here we assess the forecast for major economies, drawing insights from our regional portfolio committees and investment professionals.

U.S.: Record-breaking recession and policy response

Tiffany Wilding

We expect the U.S. economy to experience a sharp recession in the first half of 2020 as widespread nonessential business closures necessary to slow the spread of COVID-19 curtail U.S. activity with unprecedented speed and severity. Our expectation for a peak-to-trough contraction of around 10% in quarterly GDP (not annualized) is significantly larger than the roughly 4% peak-to-trough decline during the global financial crisis in 2008. However, we also expect the contraction to be shorter, as quarantines are eventually relaxed and monetary and fiscal policy stimulus supports the economy – with a lag. Alongside this sharp contraction, we look for the U.S. unemployment rate to almost reach 20% before moderating back to between 6%–7% by year-end (for details, see our recent blog post, "The U.S. Likely Faces a Deep Hopefully Short Recession" ).

Our forecast for a rebound in the second half of 2020 is based in part on the expected gradual easing of the pandemic and reopening of the economy, but perhaps more importantly on the unprecedented speed and size of U.S. policymakers’ economic response. In addition to cutting the policy rate to zero and restarting large-scale purchases of U.S. Treasuries and mortgage-backed securities (MBS), the Federal Reserve has steadily rolled out programs aimed at reducing financial market stress and maintaining the flow of credit to households and businesses. Congress also worked quickly to pass a record $2.2 trillion dollar stimulus package, which includes 6% of GDP in spending to directly support individuals and businesses. Further fiscal stimulus is likely to be passed in the next few months.

Despite unprecedented efforts by policymakers, we still see clear downside risks to the forecasts. First, uncertainty about the spread of the coronavirus remains high. A second wave of cases or a slower path to reopening the economy would prolong the economic pain. Second, while policymakers have been quick to react to worsening economic conditions, any delays in dispersing funds throughout the economy raise the risk that bankruptcies lead to longer-term economic damage.

Canada: Dual shock and downside risks

Tiffany Wilding

We expect Canada to experience a sharp recession in the first half of 2020, as dual shocks hit its economy. Widespread nonessential business closures necessary to bolster the health of Canadian residents have already affected an estimated 5.4 million Canadian jobs, and curtailed activity. And, as the energy sector makes up a relatively large portion of Canadian GDP (8%) and capital expenditures (18%), the large drop in energy prices will likely exacerbate the growth contraction.

We expect peak-to-trough contraction of around 15% in Canada’s quarterly GDP (not annualized), which is significantly larger than the roughly 4% peak-to-trough decline during the global financial crisis in 2008–2009. Government and central bank measures to support households and businesses, including 5% of GDP in direct government transfers, are expected to contribute to a rebound in activity in the second half of 2020, leaving full-year growth down roughly 8%. Still, the Canadian recovery is expected to be slower and the downside risks are greater due to a starting point of relatively high household leverage, and the subsequent need to deleverage as households adjust to lower incomes.

Euro area: In a deep plunge amid coordination issues

Nicola Mai

The euro area looks set to experience a short, but very deep recession, with full-year GDP declining nearly 10% in 2020. The level of activity looks set to fall around 20% (non-annualized) during the first half of 2020 before starting to normalize. For reference, the peak-to-trough decline in quarterly euro area GDP was around 6% in 2008–2009.

While we forecast gains in GDP to be robust in the second half of 2020, they build on a depressed starting point, implying that activity will still be around 5% below its 2019 peak by year-end, and that it likely will not return to pre-COVID levels until 2022. The slow normalization comes from the need to relax lockdowns gradually, and from the collateral damage of the crisis through behavioral changes, damaged animal spirits, corporate defaults, and higher unemployment (which we expect to be above 10% by year-end).

Some of the collateral damage will be mitigated by policy responses. We think euro area governments may end up tripling current fiscal easing efforts of around 2% of GDP in aggregate, which will go on top of nearly 20% of GDP worth of guarantees and liquidity measures for companies. We see the euro area fiscal deficit rising to above 10% of GDP, reasserting the need for the European Central Bank (ECB) to continue to anchor sovereign balance sheets. We think the central bank will do what is needed, and add to its purchase programs if necessary. Our expectations for a centralized pan-European fiscal effort, on the other hand, are modest, reflecting all-too-common political coordination issues.

Uncertainty around these macro estimates is high. On balance, we see risks as skewed to the downside given possible delays in containing the virus, the risk of a second wave of infections, and the potential for a slower recovery on the back of damaging second round effects from the crisis.

U.K.: Fiscal and monetary holding hands

Peder Beck-Friis

We forecast U.K. GDP to contract nearly 8% in 2020, with activity bottoming in April before starting a sluggish recovery around mid-May. We expect the recession to be short, lasting only two quarters, but sharp, with a peak-to-trough GDP hit of 16% (non-annualized), almost three times as deep as during the 2008–2009 financial crisis. The subsequent normalization will be slow due to lingering effects, with activity likely to remain below pre-COVID levels through 2021. In our baseline forecast, the unemployment rate ends the year at close to 6%, as we expect the government’s new job retention scheme will succeed in reducing somewhat the number of layoffs. Inflation, meanwhile, is likely to remain well below the Bank of England’s (BOE) target over the cyclical horizon, as disinflationary pressure from lower oil prices and demand more than outweigh offsetting pressures from supply disruptions and a weaker pound.

The U.K. policy response has been prompt and coordinated, softening the fall and, in our view, likely preventing the shock from creating lasting damage to the supply side of the economy. We expect the government to add slightly to already announced direct fiscal measures worth 5% of GDP, bringing the overall deficit to low double-digits. That comes on top of government-guaranteed loans worth 15% of GDP. Meanwhile, we expect the BOE to remain a credible backstop for the sovereign balance sheet, keeping its policy rate at 0.1%, adding to existing asset purchases to broadly match the size of the fiscal deficit, and directly lending to the Treasury where appropriate. While negative interest rates and yield curve control are unlikely, we do not rule them out.

Japan: Monetary and fiscal policy coordination

Jun Yamamoto

We expect Japan’s GDP to decline between 3% to 4% in 2020, with economic activity bottoming in May when the state of emergency is currently scheduled to end.

We anticipate a 6% contraction between the third quarter 2019 peak to the forecasted trough – marginally smaller than the 8% peak-to-trough decline in 2008–2009.

We forecast growth to pick up during the second half of 2020, but normalization will be slow – we are unlikely to recover to pre-COVID-19 GDP levels by the end of 2021. While Japan’s state of emergency is less stringent than those seen in the West, the economic impact will still be large and broad-based. A change in consumer behavior will likely bring long-lasting damage to inbound and domestic consumption – this after Japan had high hopes for both ahead of the Olympics.

Inflation should remain low, as we see disinflationary pressures from lower oil prices and a deteriorating output gap. Meanwhile, unemployment should be above 3% by the end of 2020.

On policy, the Japanese government swiftly prepared a stimulus package of unprecedented scale: 108 trillion yen. We expect the 2020 fiscal impulse to be approximately 4 percentage points of GDP. The increase in bond issuance to finance the stimulus will require monetary and fiscal coordination. In our view, the Bank of Japan’s current yield curve control framework should be well suited for this.

Looking ahead, growth risks are still biased toward the downside. Given the uncertainty in the timing of the peak of COVID-19 cases and the possibility of a second wave, the state of emergency could be extended but not shortened. However, we expect additional fiscal stimulus if further downside risks materialize.

China: Unprecedented recession, muted recovery

Stephen Chang

COVID-19 surfaced in Wuhan last December, and on 23 January China’s central government decisively locked down Hubei province and enforced nationwide social distancing. These measures effectively flattened the contagion curve. Local transmission now appears largely contained, but the risks are not over. Many quarantine measures remain, and economic activities are normalizing slowly.

The economic loss is unprecedented: In nine weeks of lockdown, industrial production and services contracted about 10 to 15 percentage points from their pre-pandemic levels, and the unemployment rate could rise to 8%–9% from 5%. The first quarter of 2020 will mark the recession trough in China, in our view, with GDP estimated to fall 10 percentage points below its pre-COVID level. For comparison, even during the global financial crisis, China’s GDP did not contract.

Fiscal stimulus to date has increased to 16% of GDP, consisting of a 5% budget deficit, 6% in a special government bond financing investments, and the rest in liquidity/credit supports. Though the fiscal impulse could add 4 to 5 percentage points to GDP, the multiplier effects are weak for both corporate and household spending. We expect the People’s Bank of China (PBOC) to cut policy rates by 30 to 50 basis points and keep liquidity ample, while efforts to maintain stability in the yuan will be continued.

Economic activity will likely follow a U shape over the course of 2020. The global recession will hit exports primarily in the second and third quarters of 2020, domestic demand is still hampered by quarantine curbs, and stimulus transmission is weak amid spreading bankruptcies and job losses. We forecast GDP growth in 2020 will be in a broad −4% to +2% range, the first severe economic recession in China since 1976. The economy likely will not recover to the fourth quarter 2019 level until the first quarter of 2021.

Uncertainties are high and downside risks dominant: The epidemic may potentially recur in new waves, and corporate bankruptcies and job losses will be hard to reverse. Globalization and urbanization have already suffered a major setback, with trade, supply chains, labor migration, and investment flows all greatly disrupted. Productivity and job creation in the dynamic coastal area are at risk of being permanently impaired.

Disclosures

All investments contain risk and may lose value. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.