Rather than causing home prices to tumble, the sharp rise in mortgage rates over the past two years has bolstered the U.S. housing market by curbing the supply of homes put up for sale. That supply-demand imbalance is likely to continue, in our view, supporting further home price appreciation and rental inflation.

Several factors have constrained supply, including the "lock-in effect" by which homeowners with low mortgage rates are reluctant to sell to buy another home at a much higher rate. We believe this effect will persist. The construction of multifamily housing is also expected to decrease over the next few years, exacerbating the housing shortfall.

We are monitoring several gauges of incoming housing supply for signals about market health. PIMCO sees attractive opportunities in bonds backed by residential mortgages, given our expectation that home price appreciation will remain resilient. We believe U.S. home prices could rise by low double-digit percentages in total over the next three years in the current higher-rate environment.

Higher rates act as a supply constraint

U.S. housing market dynamics have changed drastically since the start of the pandemic, when monetary stimulus pushed mortgage rates to historic lows, spurring a wave of home purchases and refinancings. In subsequent months, fiscal stimulus supported the U.S. economy while Americans broadly reconsidered where they wanted to live and work, leading to unprecedented home price surges in many areas.

Since then, the Federal Reserve has hiked interest rates steeply to fight inflation, and mortgage rates have spiked to 20-year highs. With home affordability sharply reduced, mortgage purchase applications have fallen to historic lows. The seasonally adjusted annual rate of existing home sales fell to 3.79 million in October, from a pandemic peak of 6.5 million, according to the National Association of Realtors. We expect a further decline to about 3.5 million to 3.75 million.

Yet this reduced activity has not translated into a large drop in home prices. After decreasing by about 3% from 2022 peaks, home prices are now back at all-time highs nationally and in most parts of the country, according to CoreLogic. Paradoxically, in addition to a stronger-than-expected consumer, higher rates have supported the resilience in home prices, through reduced supply via the following mechanisms:

1. Lock-in effect

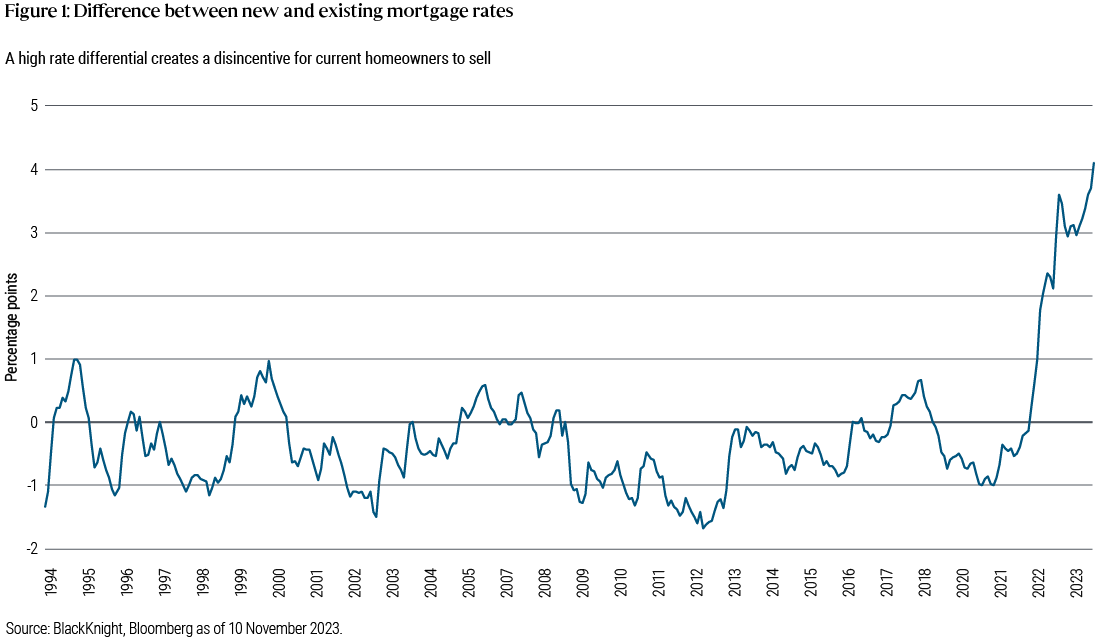

Homeowners are enjoying both strong price gains and home loans financed at negative real rates. Figure 1 shows the difference between market mortgage rates and the rates at which households financed their homes. During normal periods, this gap is less than half a percentage point. Today, it is close to four percentage points.

Any homeowner with a mortgage rate around 3% has a large economic disincentive to sell that home and buy another at a rate over 7%. In theory, this “staying in place” market should affect supply and demand equally, given that the same people who would have moved but haven’t also don’t create additional demand.

Yet we believe the disincentive of giving up a low mortgage rate also affects the number of homes that would have been placed on market due to life events (e.g. deaths, relocations, divorces), or for a move to the rental market, therefore decreasing net supply. Historically, available supply has been a key predictor of home price appreciation, leading us to expect strong appreciation given current low supply levels.

2. Construction and multifamily

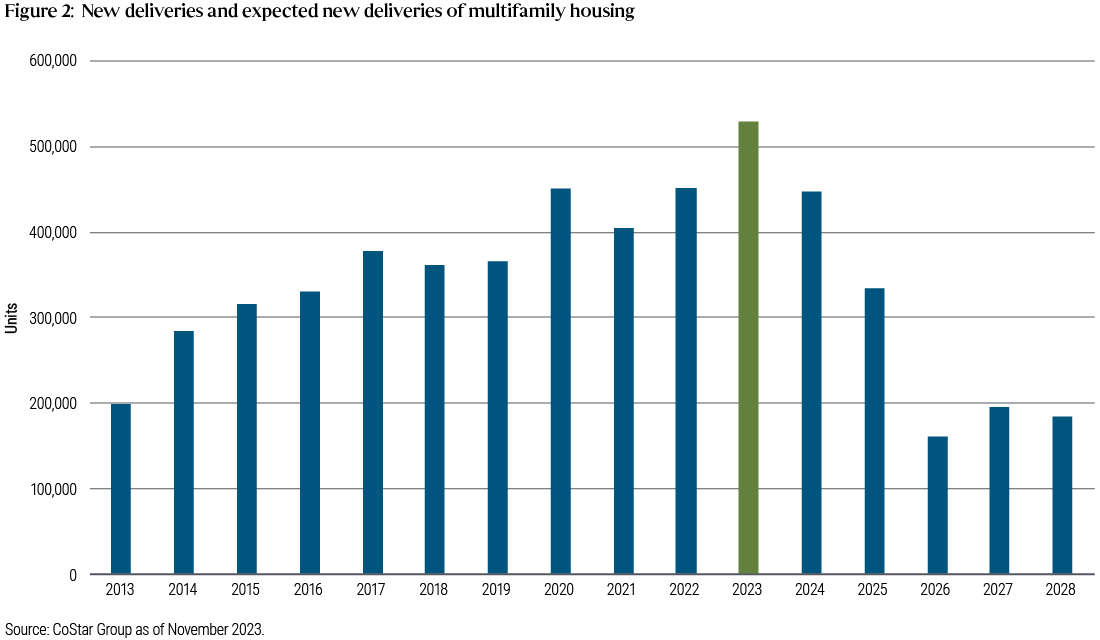

High multifamily supply has been a silver lining in the housing market, especially for renters. This year is on pace for record delivery of new multifamily units, alleviating some rental price pressures.

However, deliveries are expected to start normalizing in 12-15 months as higher rates hinder financing of new multifamily construction (see Figure 2). In 2026 onward, this multifamily supply is slated to drop sharply, which could worsen the secular housing shortage.

3. Housing and recession

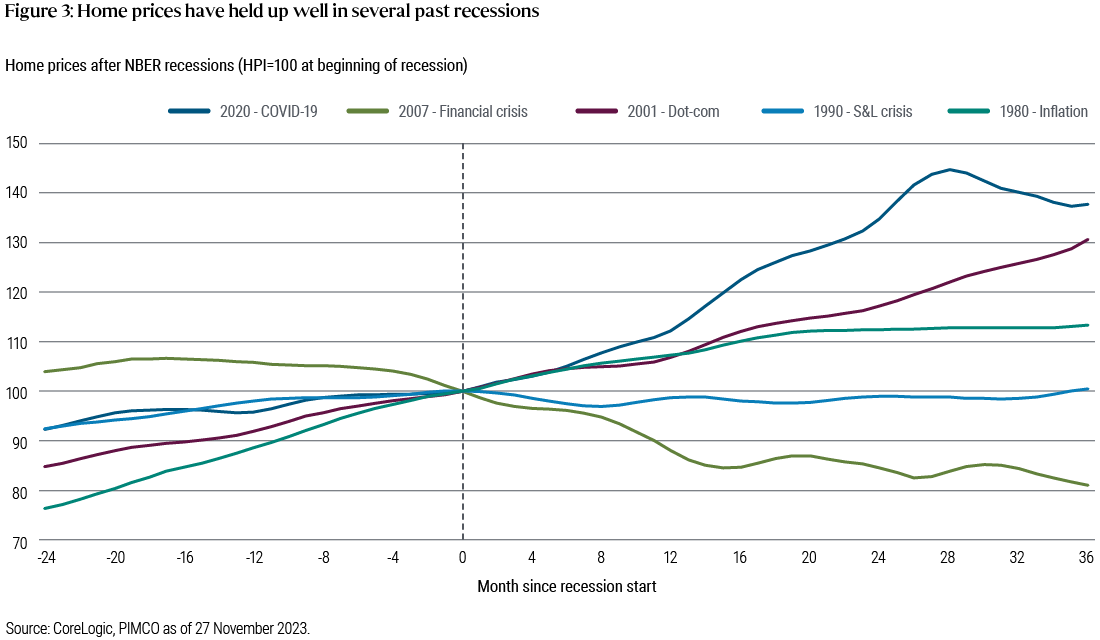

In past recessions aside from the global financial crisis, the housing market has generally held up well (see Figure 3). This is in part because the U.S. Federal Reserve typically cuts interest rates in a recession, while investors seek out bonds, pushing yields lower. That passes through to mortgage rates and acts as a shock absorber for housing.

One could argue that, if a recession were to occur, the increase in supply due to an easing lock-in effect would outweigh additional demand arising from affordability gains. However, we think this is unlikely given how far out of the money current market-rate mortgages are: If mortgage rates fall to 5%, affordability for the marginal buyer would greatly improve, yet potential sellers with a 3% mortgage would remain reluctant to give that up.

4. Monitoring the supply

In this environment, we believe it is important to monitor sources of additional supply. For existing homes, we carefully watch inventories of homes for sale, the number of new listings, absorption rates, and other metrics such as the frequency of price reductions and transaction prices compared with listing prices, including at the regional and metropolitan statistical area levels.

For new homes, we favor watching inventories of homes for sale at different completion levels, as well as the rate of completions versus starts and expected household formation. Results and comments from home builders and single family rental operators can also provide useful information on the pace of supply.

Implications: Both home price gains and rental inflation can continue to defy higher rates

Considering these factors, we believe the U.S. housing supply-demand imbalance could continue to create a strong environment for home price appreciation. Rental inflation may also remain elevated relative to the pre-pandemic period, as the structural shortage of shelter continues and as affordability challenges push more households toward renting.

At PIMCO, we continue to favor bonds backed by residential mortgages. We expect home price appreciation to remain “higher for longer,” making residential credit a robust all-weather strategy, in our view.