Spotting Opportunities in the High Yield Ratings Migration

Our outlook for the high yield market for 2022 is range-bound, as rising rates are expected to be offset by strong fundamentals, favorable technicals, and a fair valuation backdrop. We believe there are opportunities for active investors, such as identifying possible rising stars – companies with high yield credit ratings that are likely to be upgraded to investment grade – well before the market does, as well as spotting companies with deleveraging catalysts that have the potential to generate above-market returns.

We expect the high yield market to follow PIMCO’s secular themes over the next five years, with returns becoming more subdued for the asset class. That said, we also expect disruption within industries and divergence among credits to result in increased spread dispersion within the market. For example, companies that have pricing power and are able to pass on higher input costs, such as raw materials and labor, appear poised to outperform price-takers.

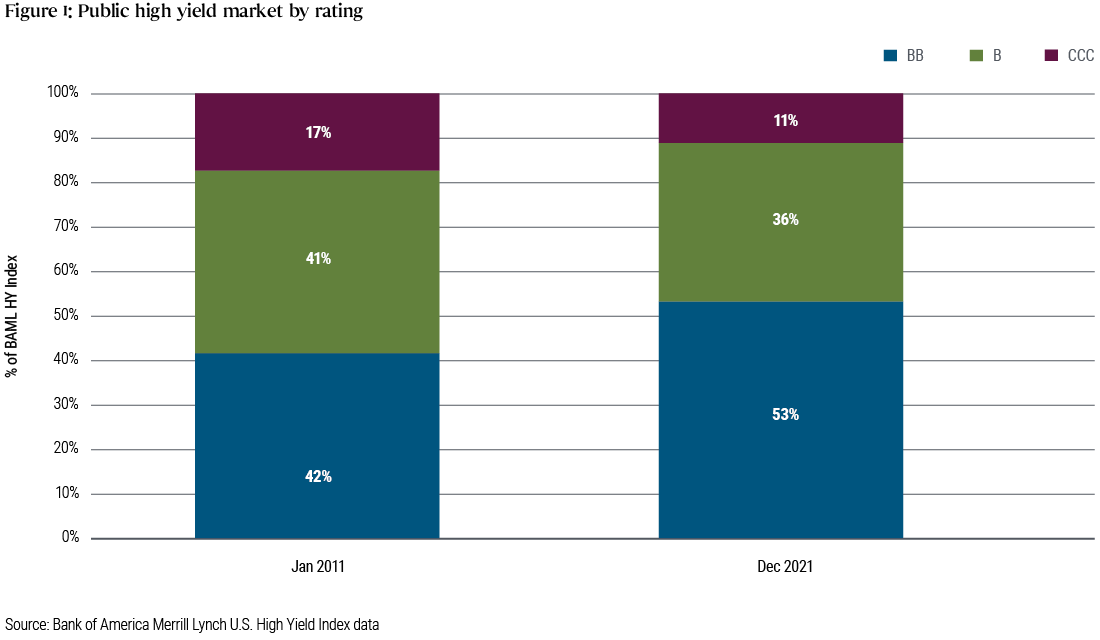

High yield moves higher in quality

The high yield market has become higher in quality in the past decade, and the COVID-19 environment has contributed to the acceleration of that trend. Ratings quality within high yield has never been higher, with over 50% of the market rated BB (see Figure 1).

If one were to overlay the ratings composition of 2011 with the current spread-per-rating cohort, the high yield market would be 50-75 basis points (bps) wider than current levels. The higher quality is also substantiated by low default rates and paltry distressed ratios. The dollar-weighted global high yield default rate ended 2021 at a record-low 0.3%, according to Moody’s, while just 1.97% of the face value of the Bank of America high yield index is now classified as distressed.

A key reason for this shift up in quality is that much of the financing for M&A and leveraged buyouts has been moving away from bonds to loan and private credit markets. Additionally, the high yield market experienced about $230 billion in fallen angel volume – the amount of investment grade debt downgraded to high yield – in 2020, according to Goldman Sachs, while many of the weakest companies defaulted.

Outlook is range-bound

For 2022, we expect high yield fundamentals to remain strong and a default rate in the low-single digits. The technical backdrop should also be favorable, as our analysis has identified $250 billion-$300 billion of notional bonds that could be upgraded from high yield to investment grade in the next 18 months. Also, J.P. Morgan estimates net supply of new bond issuance will be down 3% year-over-year in 2022, to $185 billion.

Though valuations may appear rich by some measures, the recently improved market fundamentals also appear to imply lower risk across high yield than in previous years. For example, energy tends to be one of the more volatile sectors in high yield, and that volatility is expected to be more subdued in 2022 given higher oil and natural gas prices entering the year.

We foresee two primary sources of risk in the high yield market for 2022. The first is volatility caused by expectations of rising interest rates, and the second is companies turning to shareholder-friendly actions at the expense of lenders when trying to support equity valuations.

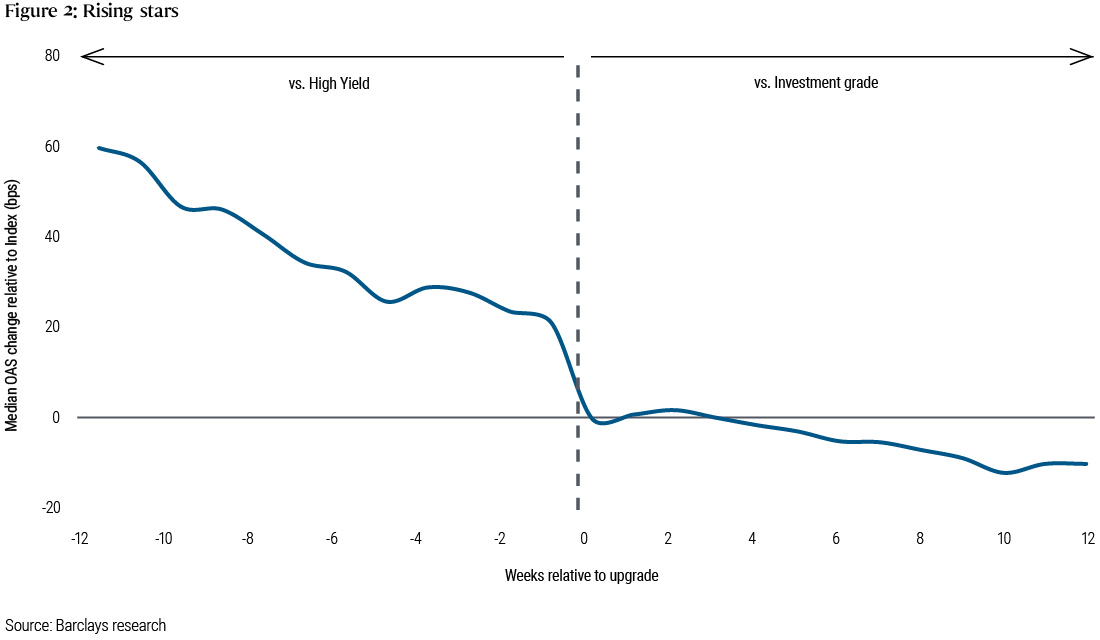

High yield in 2022, investment grade in 2023?

Although spread dispersion overall is low in the high yield market, we expect opportunities still exist for forward-looking, active investment managers. For example, when a company moves from high yield to investment grade, much of the spread tightening typically occurs six to 12 months prior to the upgrade (see Figure 2). As such, it is important to identify those rising stars before the upgrades occur and before the market widely anticipates them.

Because PIMCO uses proprietary credit ratings that can take forward-looking factors into consideration, our ratings differ about one-third of the time from those of credit-rating companies such as Moody’s and S&P. Such differentiation can be a factor in identifying rising stars well in advance of the market and benefitting from the subsequent spread tightening.

Other potential investment opportunities include looking for companies that have deleveraging catalysts, such as being bought by a larger, investment grade acquirer. PIMCO’s analysts cover credits across the quality spectrum within an industry, which can help to identify assets that could become such acquisition targets down the road.

For more on the investing landscape in 2022, see our Asset Allocation Outlook, “Opportunity Amid Transformation .”

Andrew Jessop is a managing director and high yield portfolio manager. Sonali Pier is a managing director and portfolio manager in the Newport Beach office, focusing on high yield and multi-sector credit opportunities. Sabeen Firozali is a senior vice president in the New York office, focusing on corporate credit business strategies.

Featured Participants

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

The terms “cheap” and “rich” as used herein generally refer to a security or asset class that is deemed to be substantially under- or overpriced compared to both its historical average as well as to the investment manager’s future expectations. There is no guarantee of future results or that a security’s valuation will ensure a profit or protect against a loss.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.