Canada’s Economy: Macro Challenges, Market Opportunities

- Stronger growth momentum in 2022 prompted the Bank of Canada (BOC) into a sooner and faster pace of rate hikes than what we’ve seen from the U.S. Federal Reserve (Fed). Eventually, however, the Canadian policy rate may peak modestly lower than U.S. rates.

- The BOC’s aggressive monetary tightening appears to have more of an impact on core inflation in Canada than similar central bank moves have had on other developed economies’ core inflation, and Canada’s national average housing price has dropped notably.

- Canada’s economic momentum may be slowing, and the macro outlook may be challenging, but we believe bond markets now offer compelling yields that may help investors navigate this time of uncertainty.

In 2022, the trajectories of the Canadian and U.S. economies diverged. Canada’s economy experienced stronger GDP growth as pandemic restrictions eased and the energy sector surged, while contracting fiscal policy and generally tighter financial conditions weighed on U.S. GDP. The Bank of Canada (BOC) used this positive growth momentum to accelerate its rate hiking cycle earlier this year.

As rates rise, structural differences between the Canadian and U.S. economies are also becoming clearer. Housing prices in Canada are falling more quickly and the labor market has seen a more rapid deceleration, albeit the data is volatile. Inflation – which remains uncomfortably hot for the BOC – also appears somewhat less sticky in Canada than in other developed market (DM) economies.

Given these differences and the more interest-rate-sensitive nature of the Canadian economy, we believe that terminal policy rates are likely to be modestly lower – and rate cuts may begin sooner – in Canada than in the U.S.

While this has been a challenging journey for investors, high quality Canadian bond yields now appeared poised to offer attractive opportunities, even against what is likely to be a challenging and volatile near-term macro environment.

Cyclical divergence

The Canadian economy experienced a bright start to 2022, seeing real GDP growth of 1.6% even as the U.S. economy contracted 0.6%. Alongside steady job growth, well-above-target inflation, and higher energy prices, this growth momentum through the first part of the year allowed the BOC to lead the rate hiking cycle (as we had expected; see our April 2022 blog post ). In July, the BOC gave investors a hawkish surprise, becoming the first major DM central bank in this cycle to over-deliver a rate hike relative to market pricing and the first to deliver a 100-basis-point (bp) rate increase. The BOC followed this with a 75-bp hike in September, bringing the policy rate to 3.25% (similar to the current range of 3.0%–3.25% at the U.S. Federal Reserve).

Looking ahead, with the BOC policy rate now above the terminal rate of the previous hiking cycle and with tailwinds from reopening the economy fading, momentum for the Canadian economy appears to be slowing. The labor market has stalled through the summer, and the Consumer Price Index (CPI) has surprised on the downside of consensus expectations in recent months.

More broadly, the inflation picture looks less worrying in Canada relative to other DM economies. While inflation has surged above the BOC target in Canada just as it has in other DM economies, core inflation has stabilized somewhat more in Canada in recent months. Underlying inflationary pressures also seem less worrying. Wages have accelerated less in Canada than in the U.S. given higher labor force participation and immigration. Longer-run inflation expectations have risen to levels still broadly consistent with the pre-pandemic range, in contrast to the U.S. and Euro area, where expectations have begun to tick higher. Finally, because interest rates and home prices are both direct inputs into the inflation basket in Canada, the BOC has more direct control over the inflation outlook than other central banks. Consequently, rental inflation measures – which tend to rise as housing becomes less affordable during a hiking cycle – account for only 6.6% of the Canadian CPI basket, versus 32% in the U.S.

While many uncertainties cloud the outlook, we believe the differences between the Canadian and U.S. economies suggest that the BOC is likely to deliver a lower terminal rate than the Fed for this hiking cycle. Growing economic divergence could also weigh on the Canadian dollar relative to the U.S. dollar over the cyclical horizon.

Structural differences becoming more evident

The recent inflection in Canadian economic momentum and our expectations for a lower BOC terminal rate are underscored by structural differences between the Canadian and U.S. economies. Nowhere is this more obvious than in the housing market, where higher rates have taken effect.

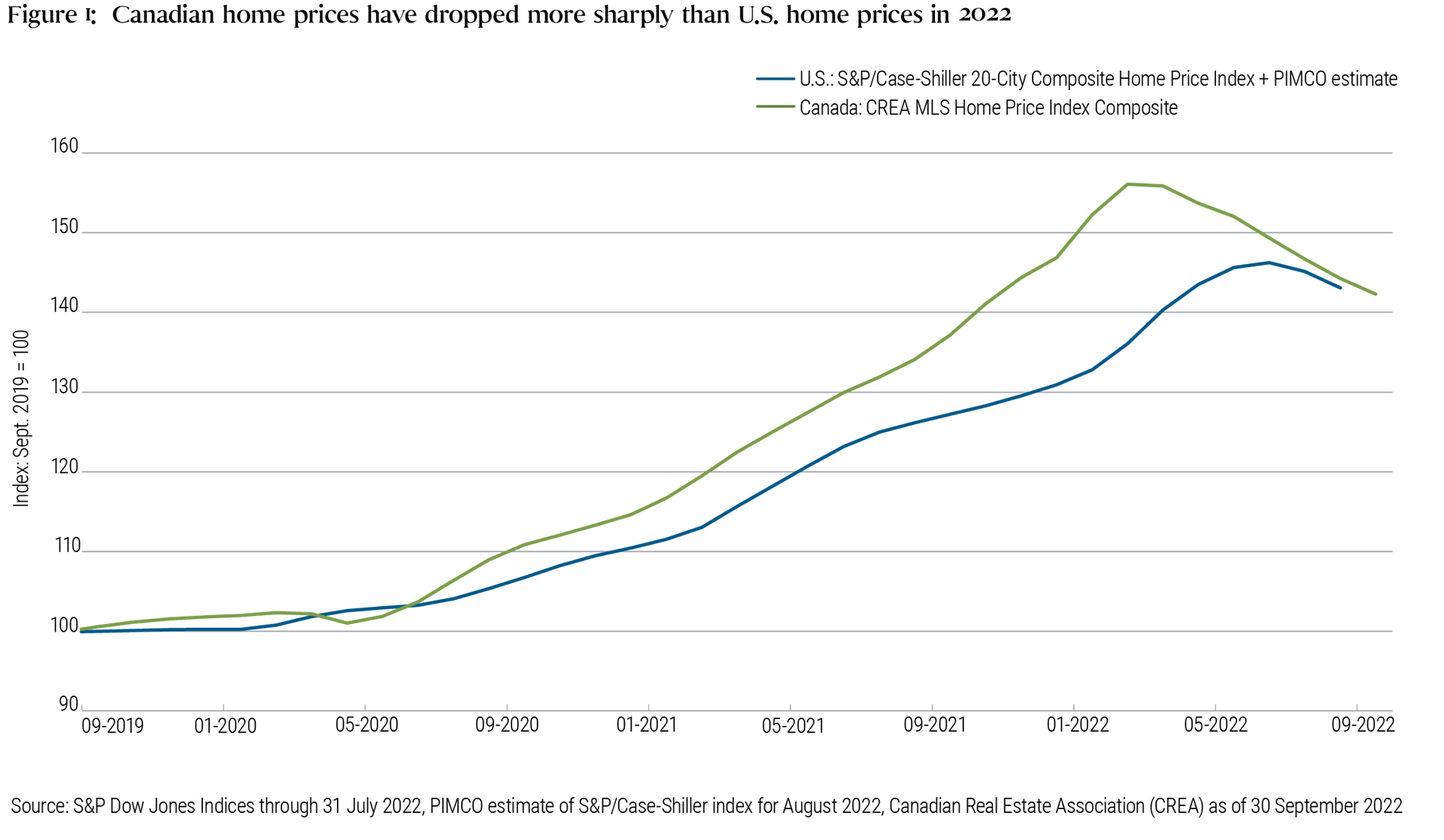

Canadian consumers have debt-to-income ratios almost twice as high as U.S. consumers, and interest rate terms for most Canadian mortgages are much shorter, typically five years versus 30 years. As a result, home prices have adjusted down much more rapidly in Canada than in the U.S. Nationwide home prices are now down about 9% from their previous highs in Canada (through September) while prices have fallen about 3% in the U.S. (based on PIMCO estimates through August) – see Figure 1.

We also believe that the structure of the Canadian mortgage market and the rapidly growing discretionary income squeeze that Canadian households will probably feel as short duration mortgages turn over suggest the BOC is likely to cut rates somewhat earlier than other DM central banks, such as the Fed, which appear focused on keeping rates steady at a contractionary level while inflation moderates.

Investment implications

As we discuss in PIMCO’s recent Cyclical Outlook Prevailing Under Pressure, we believe many of the characteristics that tend to make bonds attractive have returned along with higher yields across maturities. Investors can seek to generate higher income with bonds, and hedging characteristics are improving. Bonds and equities could become negatively correlated again in a downturn, in our view, and bond investors could essentially be paid to wait out volatility.

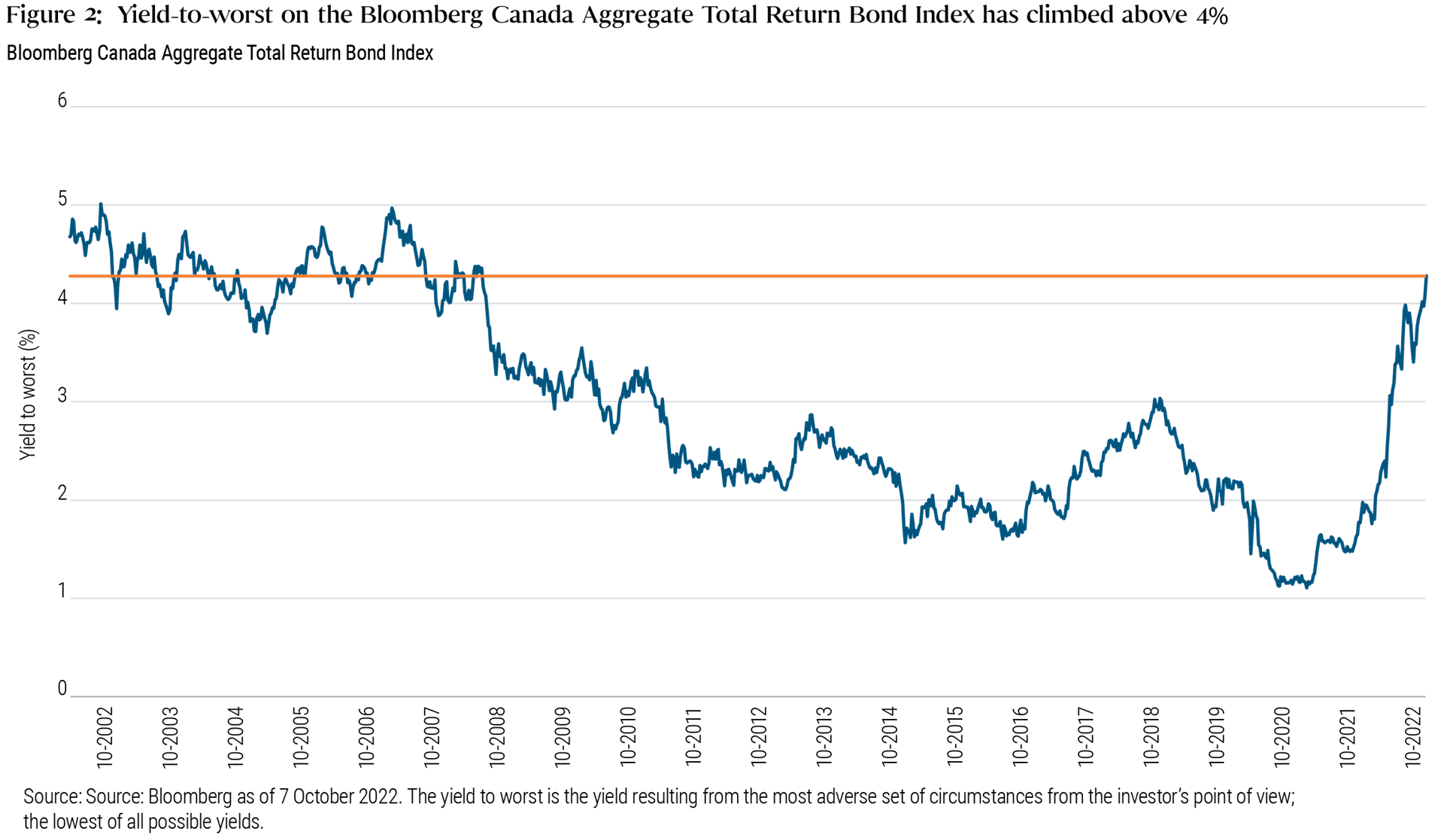

This appears particularly true in Canada, where the Bloomberg Canada Aggregate Total Return Bond Index yield, at 4.2% (as of 7 October 2022), suggests high quality fixed income yields are reaching attractive levels not seen since prior to the global financial crisis (see Figure 2).

Dispersion within markets appears high, and the potential for active selection of bonds to add value may be even higher. Amid what is likely to be a challenging macro environment over the cyclical horizon, investors may be able to seek attractive opportunities while maintaining a focus on higher quality. We believe bonds offer compelling value in these challenging macro conditions.

Featured Participants

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. There is no guarantee that results will be achieved.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the United States. The Canadian Real Estate Association (CREA) MLS® Home Price Index (HPI) tracks changes in the value of the residential real estate market across Canada. The Bloomberg Canada Aggregate Total Return Bond Index tracks the Canadian investment grade bond market. It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2022, PIMCO.