Summary

- We see diverging paths for growth, inflation, and central bank policy around the world. U.S. economic resilience will likely persist, but inflation remains a risk. Amid this outlook, our multi-asset portfolios emphasize quality and diversification.

- Top-down and bottom-up signals have us modestly overweight equities, with a focus on U.S. large cap stocks, select emerging markets, and some industrial cyclicals. Equity allocations should also help mitigate inflation risk.

- Central bank policy should bolster fixed income investments in developed markets outside the U.S., such as Australia, Canada, the U.K., and the eurozone. We also favor U.S. agency mortgage-backed securities and several areas of securitized credit, given their attractive risk/reward profiles.

The global economic and market outlook suggests diverging paths among regions and sectors. Last year, overall global growth looked stagnant, but trends this year suggest potential for a soft landing instead of a recession – mainly due to the continuing strength in the U.S. economy. But that resilience comes with risks: most notably, the potential for hotter inflation.

The diverging macroeconomic outlook creates compelling opportunities among asset classes.

In fixed income markets, we’re adding to our investments in select countries outside the U.S. where easier monetary policy this year is likely to boost bonds. And in equities, while we continue to favor high quality companies – which are poised to withstand a range of macro scenarios – we’re increasing allocations to a broader range of sectors, including industrial cyclicals. Diversification and flexibility remain crucial, and active management can help uncover intriguing ideas while managing risks.

Overall, we see a target-rich environment for multi-asset portfolios.

Macro backdrop: growth dynamics, inflation risks

Our proprietary business cycle indicator (the dynamic factor model, which incorporates around 750 macro and market variables) signals that the U.S. economy is approaching the late-cycle phase of an expansion. U.S. real GDP growth has remained robust, while inflation progress has stalled at levels running somewhat above the U.S. Federal Reserve’s (Fed’s) 2% target. As a result, U.S. policy rates are likely to remain elevated for longer than previously thought, opening the door for further tightening in financial conditions and the risk of increased volatility from areas of the economy more vulnerable to higher rates: commercial real estate, private credit, and regional banks. This means that although the factors that have contributed to U.S. economic resilience appear durable, we can’t rule out the risk of recession (for details, read PIMCO’s latest Cyclical Outlook, "Diverging Markets, Diversified Portfolios”).

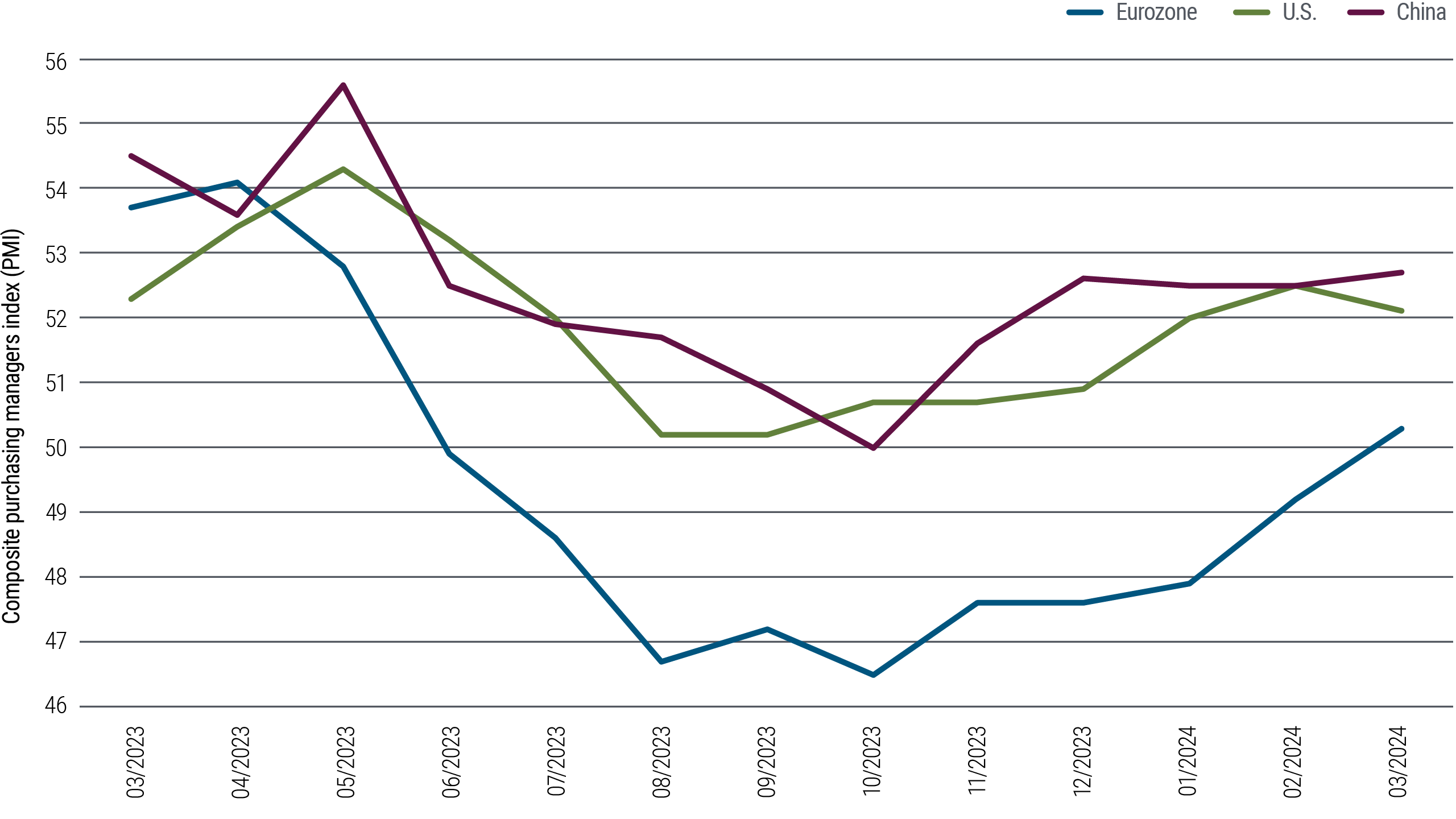

In addition to U.S. economic strength, we see some early signs of nascent potential acceleration elsewhere, after stagnant to slightly contractionary growth across developed markets (ex U.S.) in 2023. For example, purchasing managers indices (PMIs), a leading macro indicator for activity, have rebounded in some regions in the last couple of months (see Figure 1). In general, however, the U.S. likely remains the main engine for global growth, particularly relative to other developed markets.

Economic resilience doesn’t come without risks, however, especially as central banks remain focused on bringing inflation down to target levels. U.S. inflation has remained well above target this year, exceeding market expectations and likely delaying Fed policy rate cuts. This higher-for-longer interest rate scenario could potentially slow the momentum of economic growth itself.

In such an environment, companies with strong balance sheets and easy access to capital would likely fare better than smaller businesses and those more sensitive to interest rates.

Earnings cycles and equity opportunities

Macro trends and supportive bottom-up signals have us modestly overweight equities in multi-asset portfolios.

One notable signal appears in our analysis of corporate earnings calls, where we’ve observed the percentage of companies mentioning “destocking” has fallen from 27% last October to 15% in April. That suggests a marked improvement in this inventory drag, which had been a concern for many companies last year (though we note few are talking about restocking yet).

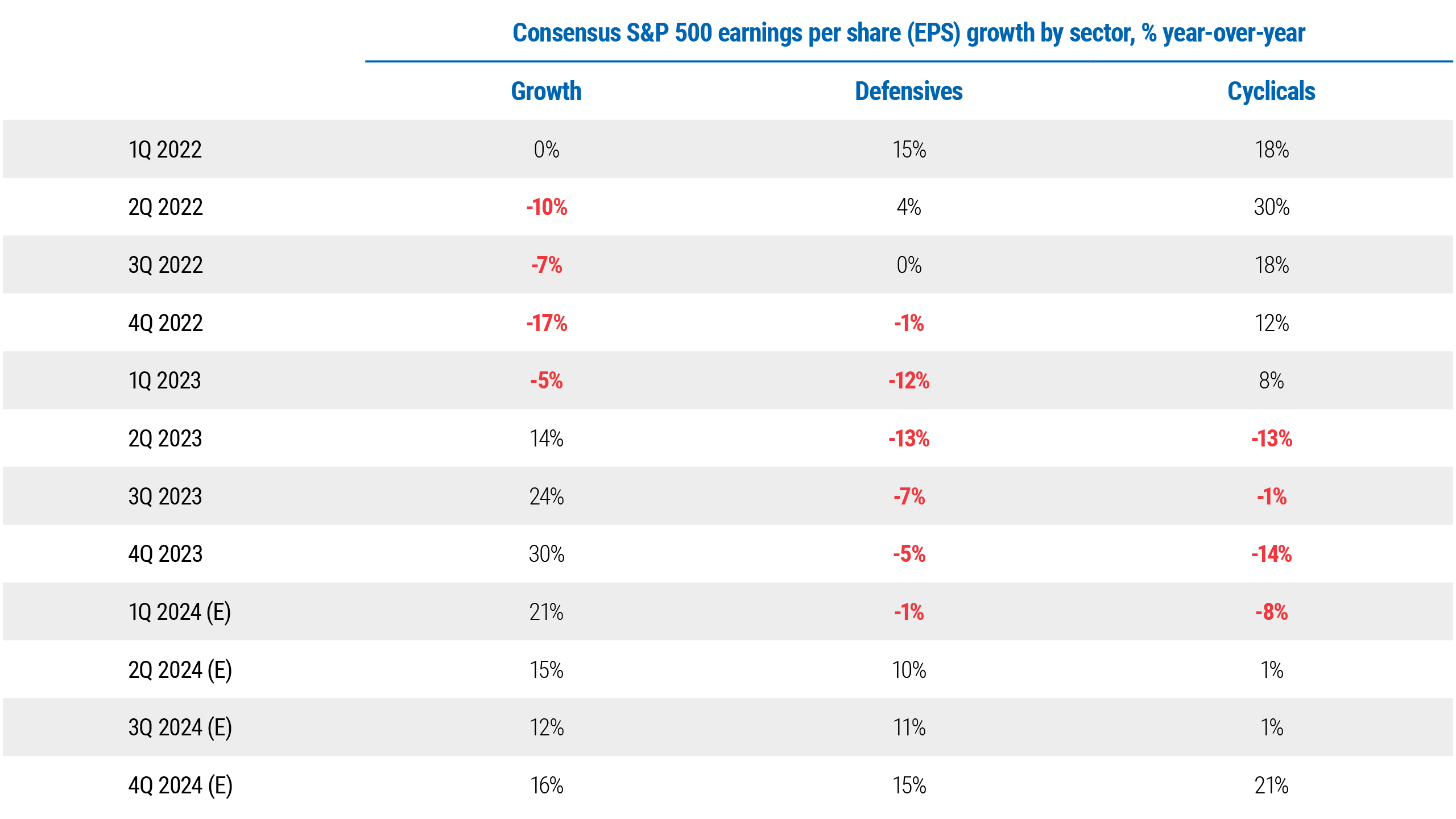

We’re also seeing a resurgence of earnings per share (EPS) as several sectors emerge from what we call “EPS rolling recessions,” whereby different equity sectors experience earnings downturns at different times and then recover, one after the other, over a span of several quarters.

Indeed, the growth sector of the S&P 500 (dominated by technology) went through an EPS recession in 2022 and then recovered in 2023 while most other sectors’ EPS were contracting (see Figure 2). As we progress through 2024, we expect defensive and cyclical stocks will emerge from their earnings contractions, potentially leading to significant price appreciation.

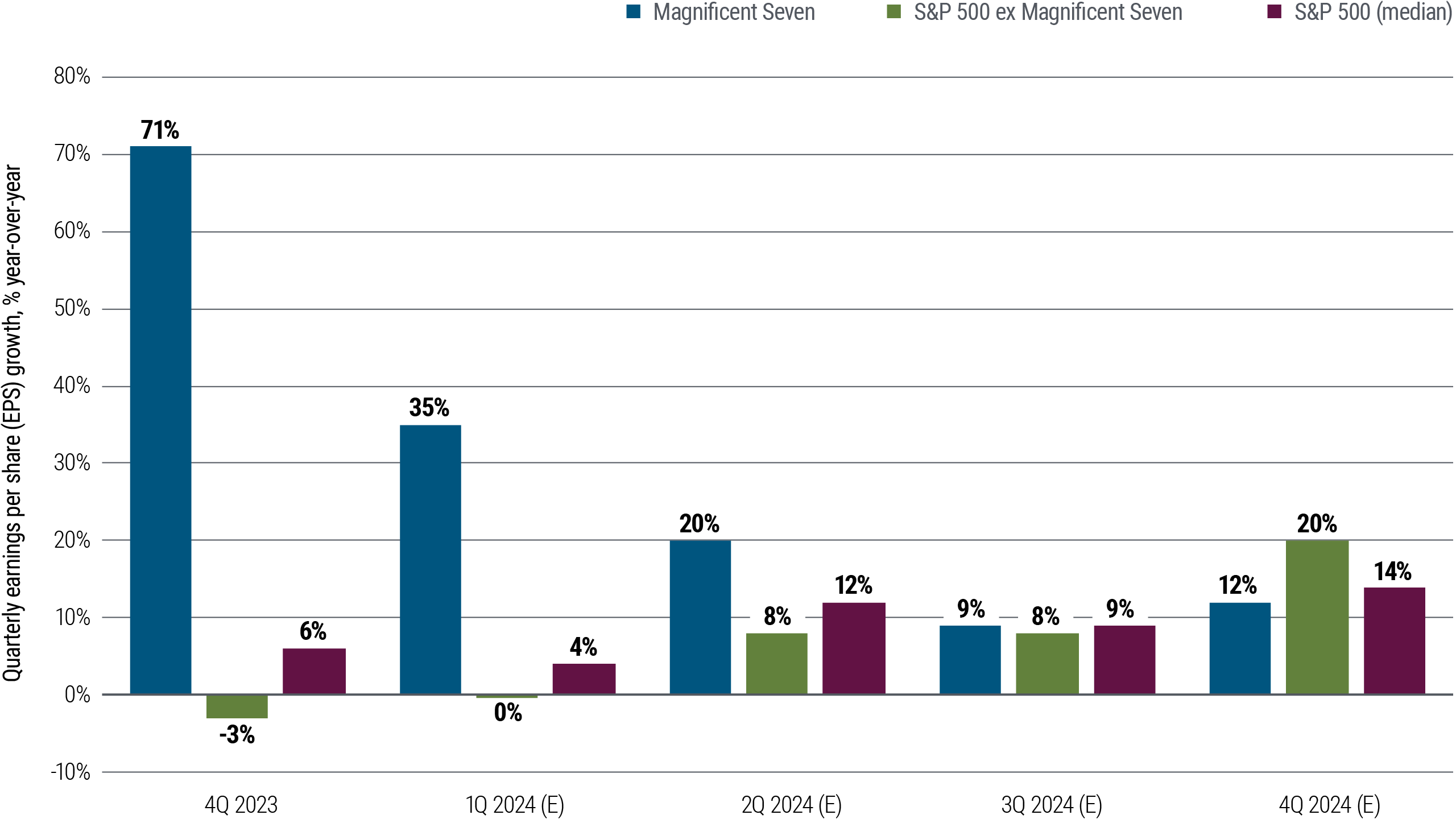

The timing of these rolling recessions and recoveries could lead to a convergence in EPS growth rates between leaders and laggards in the S&P 500. While the “Magnificent Seven” tech stocks saw 71% year-over-year EPS growth in 4Q 2023, this is expected to moderate to 12% by 4Q 2024 (see Figure 3). In contrast, for the remaining 493 stocks, earnings are projected to improve from a 3% contraction to 20% growth over the same period.

Earnings growth could be a strong support for price returns of laggards, and we expect more breadth in equity performance, versus returns concentrated mainly in the Magnificent Seven (which accounted for 5 percentage points of the 11% overall return in the S&P 500 index in 1Q 2024). Specific sectors whose earnings are likely to accelerate more this year include energy and health care. Conversely, big tech and communication services may see decelerating (yet still relatively high) EPS growth.

Turning to equity factors, late-cycle dynamics tend to bode well for quality, and to a somewhat lesser degree momentum and low volatility. This is based on our historical calculations of Sharpe ratios for various equity factors under various cycle phases for the past 40 years.

In a portfolio context, the top-down environment and bottom-up trends combine to suggest a modest overweight to equities. We favor higher-quality large cap names, particularly in the U.S., and also in select emerging markets with reasonable valuations. Industrial cyclicals may also offer intriguing opportunities as they emerge from a rolling earnings downturn.

We also believe that exposure to equity markets offers a cost-effective approach to managing inflation risk, so our asset allocation portfolios are overall neutral on real assets.

Diverging outlooks support a diversified bond allocation

We believe the elevated starting yields prevalent across much of the bond market today bode well for capital appreciation, and we tend to favor intermediate maturities. That said, as the outlook and scope of inflation, growth, and central bank policy diverge among countries, sovereign bond performance may be likely to diverge as well.

We see particularly attractive opportunities in regions where growth remains slow or stagnant and inflation is more under control, suggesting easier monetary policy ahead that could provide a strong boost to bonds. Specifically, we favor bonds in Australia, where central bankers are mindful of high household debt and variable mortgage rates. The U.K., eurozone, and Canada also show potential for earlier and more aggressive central bank easing than in the U.S., based on inflation trends and economic outlooks. Overall, this desynchronization in central bank trajectories between the U.S. and other major developed economies creates prospects for diversifying a bond allocation and seeking attractive returns.

The U.S. may continue along a strong growth trajectory, accompanied by still-high inflation. This makes U.S. bonds generally less appealing than those in many other developed markets. However, we still favor U.S. agency mortgage-backed securities given attractively wide spreads over Treasuries plus the potential for spreads to tighten once we gain more clarity on the timing of Fed rate cuts, which should reduce interest rate volatility.

In credit markets, we see attractive valuations and resilient fundamentals in several areas of securitized credit. Our portfolios are generally neutral on investment grade corporate credit given tight spreads, and are underweight high yield, as defaults may begin to rise.

In currencies, the global outlook has us favoring the U.S. dollar and select emerging markets, while we are underweight the euro.

Key themes for investors: AI

Artificial intelligence has been a significant driver of equity returns, and we expect this to continue as technologies improve and progress is made in commercial applications.

Early in 2023, the potential for AI to enable widespread productivity gains and unlock new analytical possibilities spurred significant multiple expansion (i.e., increases in valuation), especially among technology companies. Since then, we’ve seen new product launches, increasingly powerful hardware, measurable efficiency gains, and increased capital spending as companies have embraced AI capabilities. This has driven considerable earnings growth for companies in the AI infrastructure supply chain, and demand may outstrip supply for the foreseeable future. Tech companies are prioritizing AI investments, while broader surveys of CIOs indicate a rebound in tech budgets in 2024 after two years of deceleration.

Generative AI is in a very early stage. The long growth runway ahead and strong cash flows of leading players suggest we’re not seeing a bubble, despite elevated valuations. For a basket of prominent large cap AI-linked stocks, consensus estimates call for earnings growth of more than 30% in 2024 and 28% in 2025, far outpacing earnings growth estimates for the broader U.S. equities market.

Currently, AI investments are primarily in hardware, so companies selling “picks and shovels” have been the greatest beneficiaries. Examples include semiconductors, servers, networking, and data centers. One industry CEO forecasts the installed base of data centers will double over the next four or five years to $2 trillion.

As the underlying infrastructure matures, the impact of AI will broaden, and investors should seek out the next phases of the trade. The market has recognized AI’s enormous demand for power, so utilities well-positioned to supply data centers are being rewarded. Utilities, along with energy, health care, technology, and several other S&P sectors, have seen a marked increase in the number of companies mentioning AI by sector in their earnings calls.

We anticipate that future beneficiaries of the AI theme will include 1) adopters who are able to automate labor needs and drive down costs, 2) select software companies building applications for end users, and 3) biotech, given the potential for AI to dramatically speed up the drug discovery process.

Key themes for investors: U.S. election

The 2024 U.S. elections have important implications for markets at both the macro and sector levels. Neither political party has appetite for additional large-scale fiscal stimulus, nor for reforms to long-term spending. However, divergences in trade, tax, industrial, and other policy areas mean that consequences will vary based on the occupant of the White House and the makeup of Congress.

A Republican victory – whether a sweep, or just the presidency – would likely enable a policy mix that could be inflationary. We would likely see tariffs rise, prohibitions on immigration pursued, and expiring tax cuts either all or mostly extended. Sectors likely to benefit under Republican leadership include oil and gas, pipelines, autos, financials, and areas linked to defense spending. Renewable energy would face headwinds, consumer companies would face elevated tariff risk, and tech firms could be hit with negative headlines.

A Democratic victory would likely mean greater support for green energy – although fiscal space would tend to be constrained given the deficit and debt picture – and tighter restrictions on fossil fuel industries. Corporate taxes could rise, although an expansion of refundable tax credits for families could be pursued. Financial sectors could also face a tougher regulatory environment. Tariffs could be used tactically, as could export controls, but not to the extent they might under Republican leadership. A full Democratic sweep would likely lead to expansion of Affordable Care Act subsidies, which would tend to benefit the health care sector.

Takeaways

We forecast regional divergence in growth and inflation, which will prompt different monetary policy paths as well. U.S. economic strength appears poised to continue. Persistent inflation, such as what we’ve seen in the U.S. this year, remains a key risk to economies and markets.

In multi-asset portfolios, we favor higher-quality exposures and emphasize diversification. We believe U.S. large cap stocks, sovereign bond markets outside the U.S., and select securitized credit opportunities look especially attractive. Across markets, a rigorous, active approach helps us identify compelling opportunities while managing risks.

Download our investor handout for details on how we are positioning portfolios across global asset classes.

Download a PDF version of PIMCO’s Asset Allocation Outlook.