What is a bond ladder?

A bond ladder consists of bonds maturing at regular intervals, with principal reinvested into the longest-term rung as each bond matures. This approach seeks to generate a predictable income stream; it may also provide an advantage in a rising rate environment, since periodically maturing proceeds are reinvested at higher yields if market rates rise. Additionally, laddered portfolios composed of municipal bonds can be an attractive investment for investors seeking relatively stable tax-efficient income and capital preservation.

Why consider ladders?

Forecasting interest rate movements is difficult even for the most skilled fixed income investor. By investing across a range (or ladder) of maturities, laddered portfolios reduce the need to perfectly “time” interest rates. In an environment where yields are elevated and the yield curve is positively sloped, the longer rungs of the ladder bring the average yield of the portfolio higher.

Another benefit of ladders is their ability to take advantage of rising rates, through mitigating downside by investing based on a hold-to-maturity approach. This allows an investor to capture some of the potential upside by holding shorter maturity bonds that help to ensure that if and when rates do rise, there are opportunities to capture higher yields without having to liquidate existing holdings at a loss while consistently reinvesting into the longest rung of the ladder.

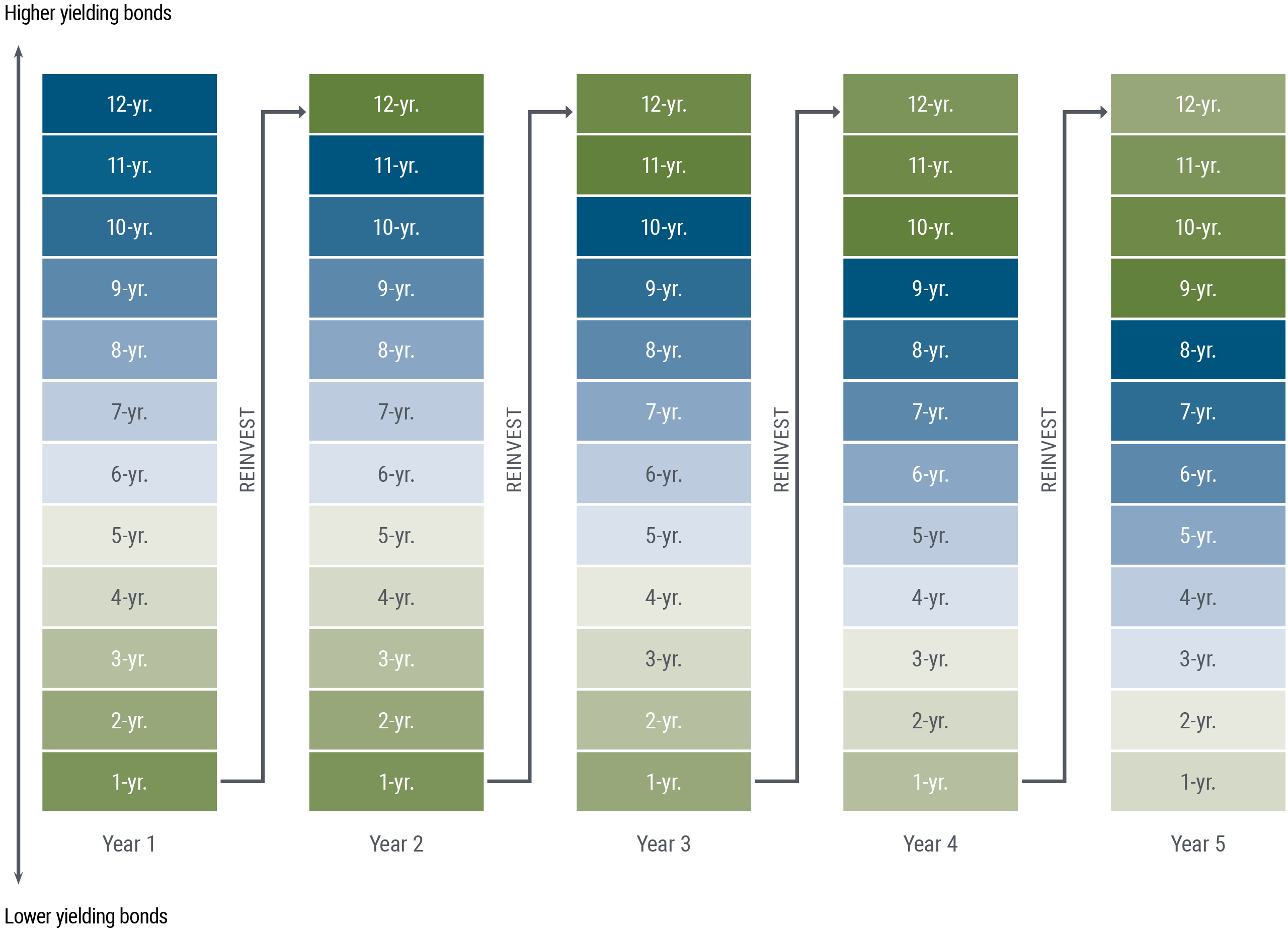

Consider that as bonds “roll down” the ladder over time, a two-year bond will become a one-year bond, a three-year bond will become a two-year bond, etc. As time passes, each rung will typically be filled, except for the longest maturity, where reinvestment will be focused as shown in Figure 1. Therefore, over time, the portfolio’s should converge toward the yield of the longest maturity bond in the laddered portfolio – this is the income stream increase over time even if market yields remain constant.

Figure 1: The Mechanics of Climbing the Bond Ladder

Source : PIMCO. For Illustrative Purposes Only

Why hire an active manager like PIMCO to build a bond ladder?

The municipal market has over 50,000 issuers, and the decline of bond insurance has made independent credit analysis essential. Rigorous fundamental credit research drives the municipal bond selection process for our ladder strategies, and our analysts develop their own internal ratings independent of the rating agencies. We monitor the quality of every credit we purchase on an ongoing and forward-looking basis, helping guard portfolios from the adverse price and liquidity impacts of a negative credit event.

Additionally, because PIMCO has over $80 billion in municipal assets under management as of March 31, 2025), we may be able to provide economies of scale in price and transaction costs that are passed on to investors. As shown in the table below, trades of $100,000 or less cost an average 56.1 basis points from January 2023 to June 2024. Institutional-sized transactions with $1 million or more have even lower cost at 17.6 bps. As such, buying in larger blocks before allocating across individual accounts can reduce transaction costs for individuals, leading to better execution and the potential for higher yields.

Figure 2: Effective Spreads by Trade Size from January 2023 to June 2024

As of 31 March 2025

Source: MSRB. There is no guarantee that institutional sized trades will result in improved pricing. Institutional sized trades are those over $1,000,000. Transaction costs are derived from MSRB analysis with data obtained from MSRB’s RTRS database.

To learn more about investing in municipals at PIMCO, please visit pimco.com/munis.