Understanding Risk Factor Diversification

What you will learn

- Why traditional asset allocation isn’t always enough

- How risk factor diversification works

- The impact of risk factor diversification on a portfolio

Risk factor diversification is a strategy of spreading the underlying risk exposures driving the return of a portfolio. While traditional asset allocation strategies seek to mitigate overall portfolio volatility by combining asset classes that don’t tend to move in the same direction at the same time, seemingly distinct asset classes may behave similarly and may not adequately diversify portfolios. Understanding risk factors that many asset classes share can help create more effective portfolio risk management.

Why is risk factor diversification important in a portfolio construction?

Risk factor diversification is important as it enables investors to pursue returns while managing risks within their portfolios. Consider that even highly diversified portfolios may not adequately cushion market volatility stemming from underlying risk factors. Understanding the risk factors many asset classes share can help to create more effective portfolio risk management.

Traditional asset allocation strategies seek to mitigate overall portfolio volatility by combining asset classes with low correlations. However, long-term trends such as globalization are driving correlations higher. As a result, seemingly distinct asset classes may behave more similarly than many investors may expect. As such, even portfolios that are well diversified across asset classes may not be positioned to adequately mitigate market volatility.

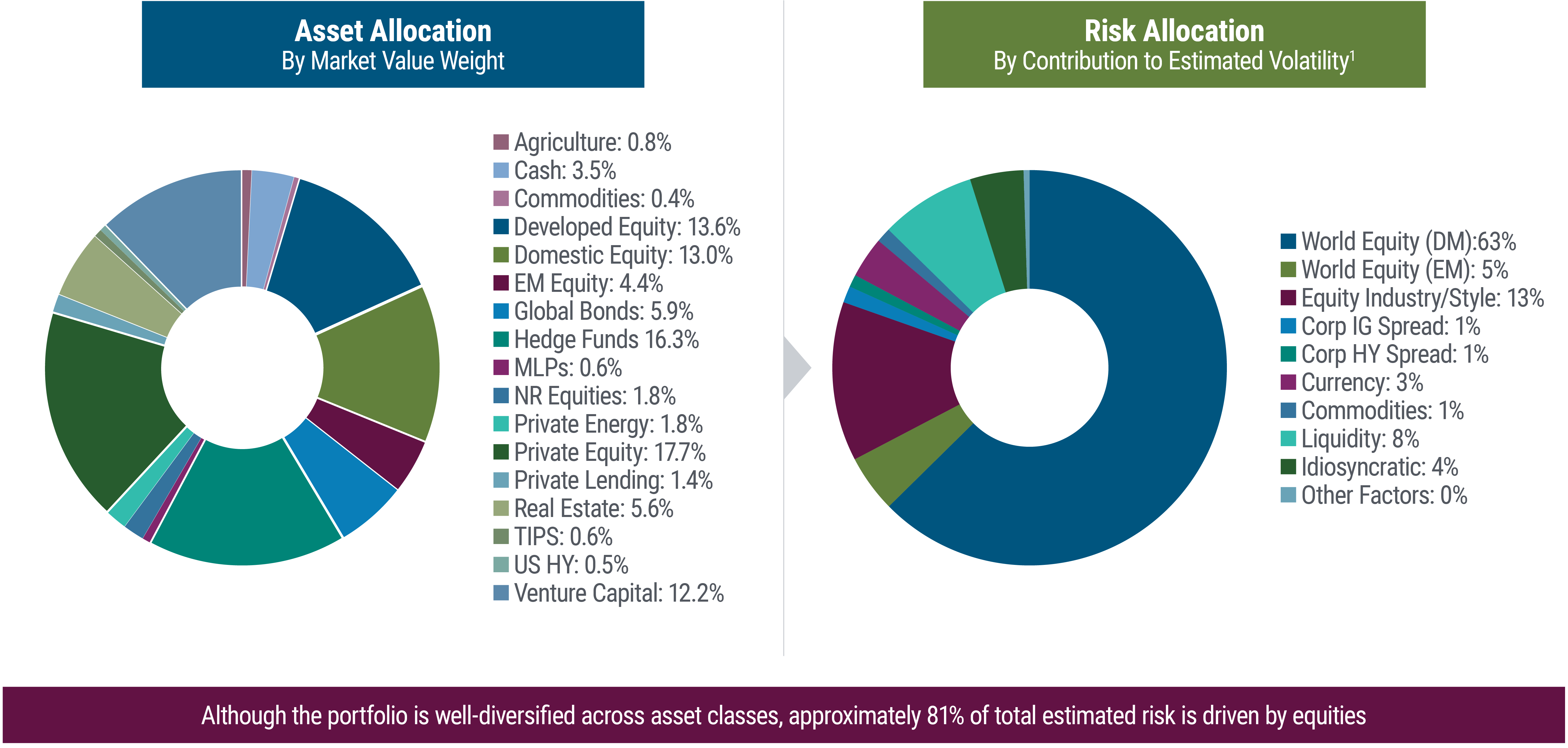

The chart on the left below shows an example portfolio that is broadly diversified across asset classes. But, as the chart on the right shows, the same portfolio actually has very concentrated exposure to underlying equity risk. Understanding these risk factors is key to creating an efficient, risk-managed allocation strategy.

For Illustrative Purposes Only.

Portfolio asset allocation information is from the 2023 NACUBO-TIAA Study of Endowments. This study is based on information collected as of 30 June 2023 based on information collected from 688 U.S. based endowments. The asset allocation percentages shown are based on the average endowment portfolio as of 30 June 2023.

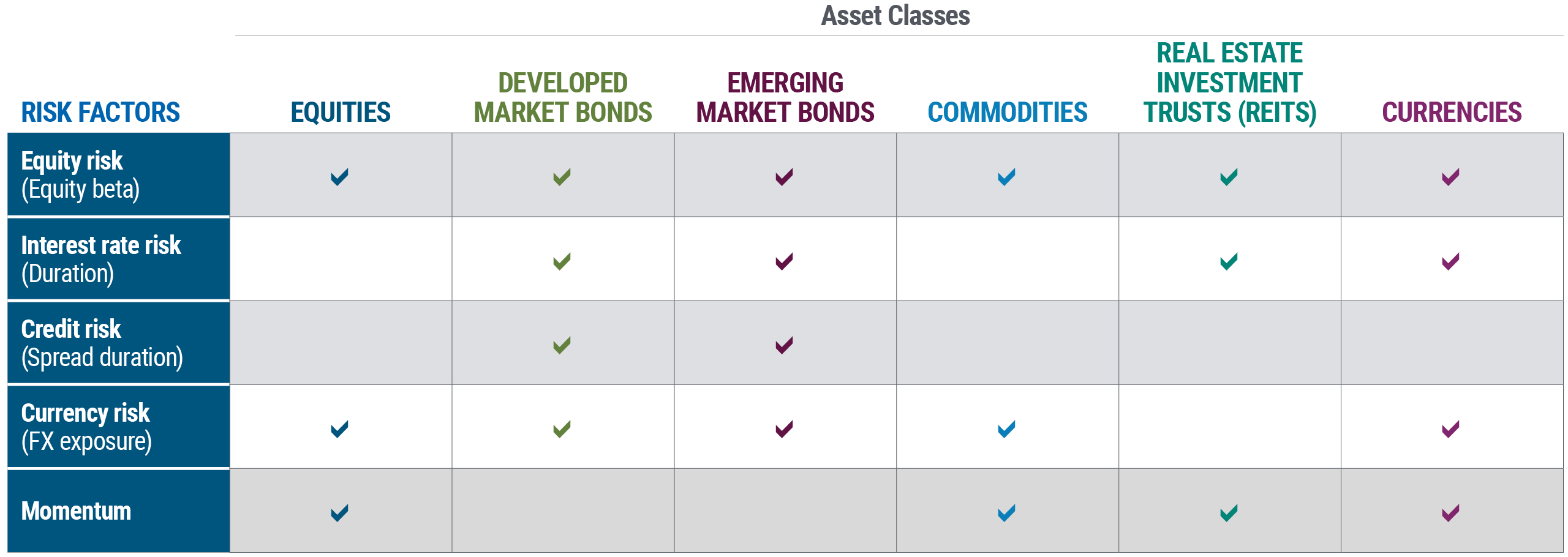

Risk factors explained

Risk factors are the underlying risk exposures that drive the return of an asset class. For example, the return from a share or stock can be broken down into equity market risk – movement within the broad equity market – and company-specific risk. A bond’s return may be explained by interest rate risk – price sensitivity to changes in rates – and issuer-specific risk. Currency risk is also a factor for assets denominated in foreign currencies.

By targeting exposure to these underlying risk factors, investors can select a mix of asset classes that provide more diversified portfolio risk.

For Illustrative Purposes Only.

Source: PIMCO. Spread duration refers to the price sensitivity of a specific sector or asset class to a 100-basis point (1%) movement in its spread relative to Treasuries.

The allocation model is based on Global Equities represented by MSCI All Country World (ACWI) Index. Fixed Income represented by Bloomberg U.S. Aggregate Index. Global Bonds represented by Bloomberg Global Aggregate USD-hedged Index. TIPS represented by Bloomberg Barclays U.S. TIPS Index. Private Equity represented by Cambridge Associate U.S. Private Equity. Hedge Funds represented by HFRI foF: Diversified Index. Real Estate represented by NCREIF Property Index. Commodities represented by Bloomberg Commodity TR Index. Cash represented by 3-Month USD Libor Index. It is not possible to invest directly in an unmanaged index.

Applying risk-factor-based diversification to a portfolio

Using an allocation strategy based on risk factors can help investors more effectively choose a mix of asset classes that best diversifies their risks, while also reflecting their views on the economy and financial markets.

For example, adding foreign currency exposure to a portfolio could be achieved by investing directly in currencies. Alternatively, it could be achieved by buying foreign equities, bonds or even commodities if valuations seemed more attractive among these asset classes. Over time, that flexibility can help add significant value to a portfolio. A professional investment manager using a risk-factor-based approach will take a forward-looking macroeconomic view on a wide range of variables, including monetary policy, currencies and economic growth trends.

Disclosures

A word about risk: All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Diversification does not ensure against loss.

The allocation models presented here are based on what PIMCO believes to be generally accepted investment theory. They are for illustrative purposes only and may not be appropriate for all investors. The allocation models are not based on any particularized financial situation, or need, and are not intended to be, and should not be construed as, a forecast, research, investment advice or a recommendation for any specific PIMCO or other strategy, product or service. Individuals should consult with their own financial professionals to determine the most appropriate allocations for their financial situation, including their investment objectives, time frame, risk tolerance, savings and other investments. Volatility is historical and is likely to change over time. Other fixed income allocations may be less volatile. Fixed income is only one possible portion of an investor’s portfolio, which can also include equities and other products. Investors should speak to their financial professionals regarding the investment mix that may be right for them based on their financial situation and investment objectives.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for Compliance Notes their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2024, PIMCO.

CMR2025-0327-4358225