Over the past few years, Alan Greenspan has become the Muhammad Ali of the financial world: the undisputed champion of U.S. stock and bond markets; the heavyweight upon whose very words and ultimate deeds swing the fortunes of millions upon millions of American and global citizens. He is in short, “The Greatest”- call him “Muhammad Alan.” Not only does he wear the championship belt of Chairman of the Federal Reserve, but much like Ali, he floats like a butterfly and stings like a bee. Trying to pin him down as to future interest rate changes can be as difficult as chasing a prize Monarch through an open meadow, but when he finally makes up his mind, his sting can be felt in every area of the U.S. economy.

Mr. Greenspan and fellow members of the Federal Reserve Open Market Committee climbed into the ring a few weeks ago and decided to raise short-term interest rates by ¼ of 1 percent. It wasn’t much of a punch – a jab instead of a haymaker left hook, and it left investors wondering whether Muhammad had lost his nerve or his legs, or whether in fact he knew something the rest of us didn’t know and was pulling his punches. The paltry 25 basis points increase wasn’t so much the problem, it was the “neutral” bias statement that followed – indicating to some that the match was over. I think not. There will be at least one and maybe two more increases in the Fed funds rate before this round of tightening is finally done.

To explain why, I think it’s important to analyze the words of Muhammad himself. That’s not so easy to do for a fighter who floats on butterfly wings, but nonetheless, the man has made so many speeches that an attempt is certainly possible. Inflation and the stability of the U.S. economy, of course, are paramount to Greenspan but the conditions that lead to low inflation and a prosperous economy can and have changed through the years. The artificial price effects of OPEC in the 1970s, for instance, helped produce an inflationary psychology that former Fed champ Paul Volcker felt incumbent to break with astronomically high interest rates in the early 80s. Greenspan, though, isn’t fighting the same opponent. Instead, Muhammad Alan is concerned about the longevity of technological productivity growth, the current state of the global economic recovery, and the wealth effect of U.S. stock and housing markets. Despite his robust denials, it’s the latter two that cause him to lose the most sleep at night, and that investors, therefore, should pay the closest attention to over the near term.

Take the global recovery for starters. Remember that in the darkest weeks and hours of the 1998 financial crisis, there was legitimate concern over the financial stability of at least several teetering emerging market countries. Russia had defaulted on its debt obligations, Brazil was on the ropes and China was rumored to be the next potential knockdown. Into this mauling stepped Alan Greenspan with a series of three ¼ of a point cuts in short-term interest rates. Although our own U.S. stock market was wobbly, the American economy was doing just fine - it was the rest of the world that was on the canvas. And so the Fed cut interest rates, not to save U.S. jobs or profits in the short-term, but to signal to other countries that we had become partners in this new-age global economy. Our prosperity over the long-term depended upon their health, and vice versa, Greenspan reckoned.

This move, although not explicitly acknowledged by the Champ in public testimony, was a stunning change of tactics. Heretofore, the Fed’s sole focus had been on domestic inflation and the welfare of American workers and businesses. Now, by cutting rates in the midst of a global crisis that was having little impact between the ports of New York City and Los Angeles, Greenspan was extending the ropes and expanding the ring to include additional countries and continents in his decision- making. It was only natural, then, as emerging nations came back to life over the past six months, as Europe showed signs of renewed growth, and as Japan demonstrated its most positive quarter of economic numbers in several years, that Greenspan would “take back” at least one of those ¼ of a point cuts in rates that were deemed necessary during the dark days of 1998.

The global crisis, however, remains fragile and the fear of another round of knockdowns is the primary reason why the Fed has stopped short of rescinding all of the decreases that took place nine months ago – at least for now. Where we go from here depends importantly on the strength of the U.S. economy and, of course, the vitality of the U.S. stock and housing markets, because they are intertwined, like the grasping arms of Tyson and Holyfield, in a clinch. The fact is that here in the U.S., soaring stocks and Internet mania have led to the largest short-term creation of wealth in this century. While those profits have not fallen into the pockets of all Americans equally, enough of them have been realized to raise our domestic GDP by nearly 4% annually for the past several years – 1% more than would otherwise have been the case. Some would argue, especially Ronald Reagan supply side conservatives, that growth is good for inflation and the more the better. Greenspan himself in the past few years has come to accept the theory that a portion of that 1% or more above average growth is due to productivity enhancements arising out of technological innovation, and is therefore non-inflationary. But the risk remains that another chunk of the growth fueled by our booming stock market may eventually lead to higher inflation. With our unemployment rate approaching 4%, the U.S. economy may be running out of workers, which would allow the existing workforce to demand higher and higher wages, leading to accelerating inflation. It is the U.S. inflation rate which has historically been the focus of the U.S. Federal Reserve, and even though the global economy has now caught the corner of his eye, Greenspan knows that the Fed cannot sit idly by and watch domestic price increases return to the days of the 1970s and 80s.

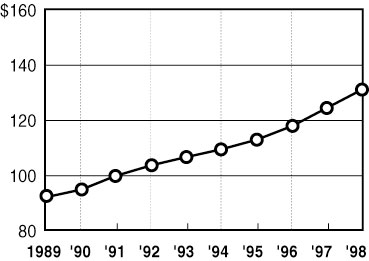

The wealth effect identified predominantly with soaring stocks is also being fueled by escalating home prices. As pointed out in a recent Wall Street Journal article by Tristan Mabry, rising home values shown in the following chart, have made it possible to refinance existing home mortgages at lower interest rates and with increasing amounts of debt.

While home prices have been going up in fits and starts for decades now, a 1997 change in tax laws made it possible to shelter the first $500,000 of capital gains from the sale of a home. Since then, the Federal Reserve estimates that individual home sales have yielded an average of $35,000 in capital gains for a total economic impact of $150 billion annually. Lower interest rates then, including the three ¼ of a point cuts made by Greenspan in 1998 to fend off the global financial crisis, have led to higher mortgage debt, higher home prices, and the use of sale proceeds to fuel consumer spending at almost all socioeconomic levels.

U.S. Home Prices

(in thousands)

Figure 1

Source: Wall Street Journal, July 6, 1999

The direction and ultimate level of U.S. interest rates, then, rests now on the gloves of three new entrants into the ring of Federal Reserve policy-making. In addition to (1) the revival and strength of the global economy, short-term Fed funds rates now depend on (2) the level of the stock market and (3) the state of the housing market. Of these three, only housing starts appear to be weakening, (although housing prices continue upward). If Japan, Europe and emerging nations continue to recover and U.S. stocks fail to cool off, Greenspan will have no other choice but to take back the remaining 50 basis points in yield cuts offered up to save the world only nine months ago. I’m betting that he will have to do just that. What happens thereafter will depend upon the existing trend of inflation, the strength of the U.S. economy, and, of course, the condition of the three new combatants described above.

Whatever the outcome, it is important to recognize that “Muhammad Alan” is fighting a new age match unlike the bouts of yesteryear. Much like Ali introduced the tactics of jab and weave and the “rope a dope,” Greenspan has recognized the importance of productivity and technological advances in keeping inflation low. And while he now downplays the significance of the global economy and the wealth effect in current policy-making decisions, I have little doubt that this new age fighter can recognize these significant punches when they’re coming his way. If so, he may be able to preemptively avoid a knockout of the building U.S. asset bubble and remain “the greatest” for as long as he wants to keep on fighting. If not, he risks his reputation and the U.S. economy’s long-term health which floats currently not on butterfly wings but on the rising tide of U.S. stocks and housing prices.

William H. Gross

Managing Director