What is a benchmark?

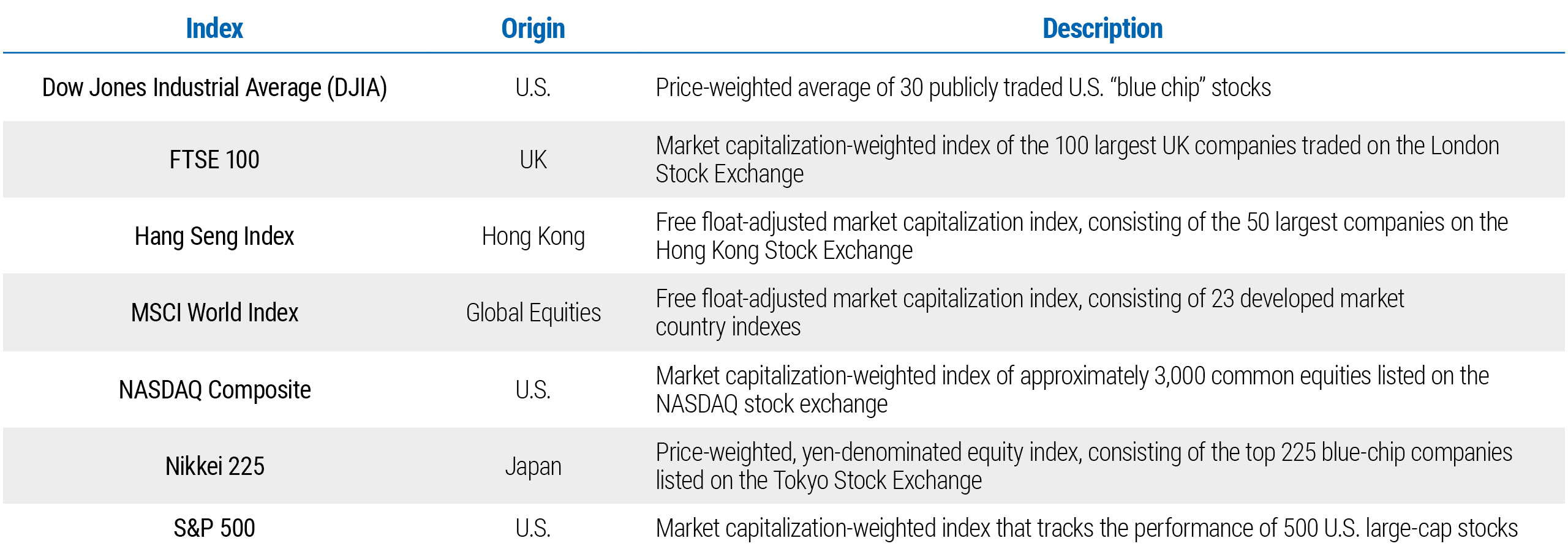

A benchmark is often a market index, or combination of indexes that investors and portfolio managers use to measure an investment portfolio’s performance. An index tracks the performance of a broad asset class, such as stocks of companies listed on stock exchanges. A narrower slice of the market, such as “blue-chip” stocks, can also have its own index, as shown in the table below.

Can I invest in an index?

Investors cannot invest directly in an index because they are unmanaged. The returns of index constituents are tracked on a buy-and-hold basis. No trades are made to reallocate to securities that may be more attractive over different market cycles or market events.

Indexes represent a “passive” investment approach and can provide a good benchmark against which to compare the performance of an actively managed portfolio. Using an index, it is possible to see how much value an active manager adds and what investments generated value.

What are the types of market indexes?

In addition to the indexes included in the table above, several other equity indexes have been designed to track the performance of various market sectors and segments. Because stocks trade on open exchanges and prices are public, the major indexes are maintained by publishing companies like Dow Jones and the Financial Times, or the stock exchanges.

Fixed income securities do not trade on open exchanges, and bond prices are therefore less transparent. As a result, the most commonly used indexes are those created by large broker-dealers that buy and sell bonds, including Citigroup, J.P. Morgan, and BofA Merrill Lynch. Widely known indexes include the Bloomberg U.S. Aggregate Bond Index, which tracks the largest bond issuers in the U.S., and the Bloomberg Global Aggregate Bond Index, which tracks the largest bond issuers globally.

Additionally, bond firms have created several indexes, providing a benchmark for virtually any bond market exposure an investor might want. New indexes are often created as investor interest grows for different types of portfolios. For example, as investor demand for emerging market debt grew, J.P. Morgan created its Emerging Markets Bond Index in 1992 to provide a benchmark for emerging market portfolios.

Indexes also exist for other asset classes, including real estate and commodities, and these may be of particular interest to investors concerned about inflation. A couple of examples are the Dow Jones U.S. Select Real Estate Investment Trust (REIT) Index and the Bloomberg Commodity Index.

What are the methodologies used to create indexes?

The major index providers use specific, predetermined criteria, such as size and credit ratings, to determine which securities are included in a particular index. Index methodologies, returns and other statistics are usually available through the index publisher’s website or through news services such as Bloomberg or Reuters.

Instead of averaging stock or bond prices, indexes typically weight each component; the most common weighting is based on market capitalization. Companies with more equity or debt outstanding receive higher weightings and therefore have greater influence on index performance. As a result, big price swings in the stocks or bonds of the largest companies can create big price movements in an index.

To reduce the volatility that may result with market-capitalization weighting and potentially improve performance, alternative indexing methodologies have emerged in recent years. Among these, fundamental indexing, developed by PIMCO sub-adviser Research Affiliates, selects and weights companies using fundamentals such as sales, cash flow, book value and dividends.

Bond indexes using market-capitalization weighting can have a troubling twist: The most influential, or largest, components may also have the biggest debt loads, which can be a sign of deteriorating finances.

How are benchmarks used to track performance?

The difference between the performance, or investment return, of an individual portfolio and its benchmark is known as tracking error. Typically reported as a standard deviation percentage, tracking error may be positive or negative.

When a portfolio is actively managed, tracking error may reflect the investment choices made by the active manager in an attempt to improve performance. If the active manager is successful, tracking error is positive and the portfolio outperforms the benchmark; if not, the portfolio underperforms its benchmark.

An investment portfolio, whether actively or passively managed, may hold securities different from its benchmark for other reasons. For example, the benchmark may contain so many securities that it is impractical to hold them all, or it may contain securities that are hard to buy, prompting the portfolio manager to substitute similar securities. In either case, tracking error may result.

Tracking error can also occur when the components of an index change. A bond may be replaced in an index due to a credit downgrade or a stock may be replaced with that of a faster-growing company. Active managers replicating such changes incur trading costs, while the indexes do not, thus creating tracking error. Active managers also may choose to make “off benchmark” allocations to certain sectors in an effort to outperform the benchmark index.

How do I select a benchmark?

With a vast number of benchmarks to choose from, deciding which one, or which combination of indexes to use, can be challenging. Here are some key questions to answer before you choose.

What are your overall performance goals, and what is your tolerance for volatility, or risk?

Investors should evaluate their return goals and risk tolerance before selecting an index. An investor with a low risk tolerance will most likely select an index with a shorter duration or higher credit quality. An investor looking for a high return may select an index with a track record of high long-term returns, which might also exhibit performance volatility and carry the chance of negative absolute returns over shorter time periods. If the portfolio is intended to offset liabilities that change with interest rates, the most important consideration when selecting a benchmark might be the benchmark’s interest rate sensitivity (or duration), rather than its prospective returns.

What is your need for liquidity?

An investor looking to invest operating cash that is used to meet short-term liabilities or obligations will need a highly liquid portfolio and would most likely select an index with a very short duration. This type of investor would want to stay away from riskier benchmarks that contain less liquid securities and exhibit greater interest rate sensitivity. Cash investors may also select custom benchmarks designed to match their liquidity profiles.

Are you planning to invest in international securities?

Because foreign currency exposure can affect the value and the volatility of a portfolio, global securities can serve two distinctly different purposes, depending on whether the foreign currency exposure is hedged or unhedged.

A global investor who wants to take a position on currency by investing in foreign holdings would use an unhedged index – one that is exposed to changes in currency values. For example, an investor who believes that the U.S. dollar will weaken may choose to invest in securities denominated in other currencies because they will increase in value if the dollar falls. However, investors seeking capital preservation or to meet liabilities typically opt for indexes that hedge currency risk and avoid the volatility that currency investing can bring.

Do you have liabilities that are linked to inflation?

Rising levels of inflation can erode the real, or inflation-adjusted, returns on an investment. A fixed income investor with inflation-linked liabilities might therefore choose, for example, the Bloomberg Euro Inflation-Linked Index, made up of eurozone inflation-linked bonds whose principal and interest payments rise with inflation. Indexes tracking the performance of specific investments that tend to benefit from inflation, such as real estate and commodities, can serve as benchmarks for portfolios invested in these assets, including the Dow Jones U.S. Select Real Estate Trust (REIT) Index and the Bloomberg Commodity Index.

How many different types of securities do you want your portfolio manager to be able to invest in?

A benchmark should be a “good fit” for your portfolio and your investment manager in terms of the range of securities in which it can invest. A broad investment universe can potentially help increase return and reduce volatility. If the benchmark is “too narrow,” however, it may be difficult for the investment manager to make noticeable contributions to the portfolio’s overall performance through active management.

Are there benchmark standards to consider?

Selecting a specific benchmark is an individual decision, but there are some minimum standards that any benchmark under consideration should meet. To be effective, a benchmark should meet most, if not all, of the following criteria:

- Unambiguous and transparent– The names and weights of securities that constitute a benchmark should be clearly defined.

- Investable– The benchmark should contain securities that an investor can purchase in the market or easily replicate.

- Priced daily– The benchmark’s return should be calculated regularly.

- Availability of historical data– Past returns of the benchmark should be available in order to gauge historical returns.

- Low turnover– There should not be high turnover in the securities in the index because it can be difficult to base portfolio allocation on an index whose makeup is constantly changing.

- Specified in advance– The benchmark should be constructed prior to the start of evaluation.

- Published risk characteristics– The benchmark provider should regularly publish detailed risk metrics of the benchmark so the investment manager can compare the actively managed portfolio risks with the passive benchmark risks.

What are the risks?

With benchmarks today covering all types of assets and investment strategies, investors should carefully consider the underlying risks in a benchmark, or index, and their risk tolerance when evaluating an index. Investors should also be aware of the holdings in their portfolios compared with those in their benchmarks to understand why their portfolios may perform differently. All investments contain risk and may lose value.