What are high yield bonds?

High yield bonds are debt securities of corporate bonds rated below BBB− or Baa3 by established credit rating agencies. They can play an important role in investor portfolios as these bonds typically offer higher coupons than government bonds, and high-grade corporate bonds (or, corporates). High yield bonds also have the potential for price appreciation in the event of an improvement in the economy, or performance of the issuing company. However, if these conditions worsen, then prices can also go down.

The high yield sector generally has a low correlation to other sectors of the fixed income market. They are also less sensitive to interest-rate risk. Due to these factors, an allocation to high yield bonds may provide portfolio diversification benefits. In addition, high yield bond investments have historically offered similar returns to equity markets, but with lower volatility.

What makes a bond high yield?

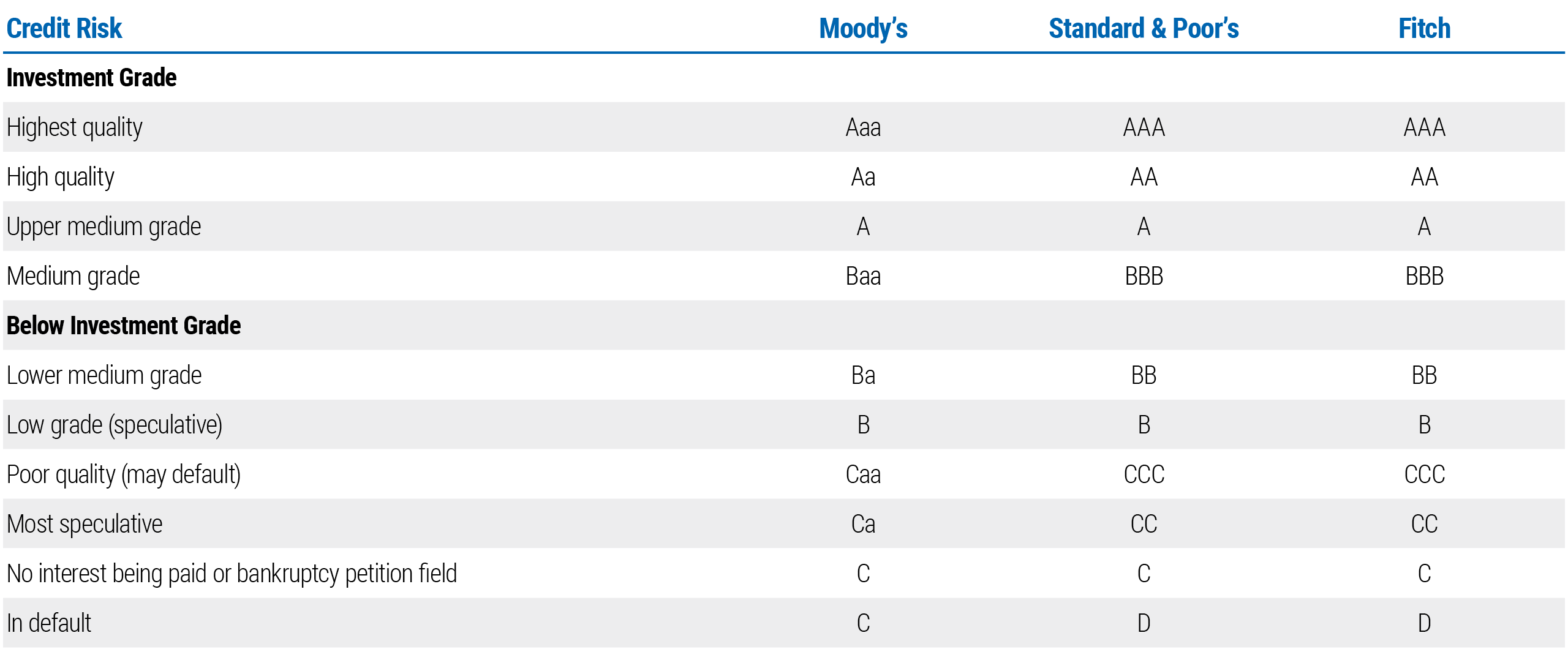

Credit rating agencies evaluate bond issuers and assign ratings, as shown in the table below. Issuers are rated on their ability to pay interest and principal as scheduled. Those issuers considered to have a greater risk of defaulting on interest or principal repayments are rated below investment grade (see table below). These issuers must therefore pay higher coupons to attract investors to buy their bonds.

High Yield Bonds

Source: Moody's, Standard & Poor's, Fitch

*The ratings from Aa to Ca by Moody's may be modified by the addition of a 1, 2, or 3 to show relative standing within the category, e.g., Baa2

The ratings from AA to CC by Standard & Poor's and Fitch may be modified by the addition of plus (+) or minus (-) sign to show relative standing within the category e.g., A-.

While agency credit ratings define the high yield market, and many investors rely on these ratings in their portfolio guidelines, investors may also conduct independent credit analysis of company fundamentals and other factors to form their own conclusions about a security’s risk of default.

Who issues high yield bonds?

Until the 1980s, high yield bonds were simply the outstanding bonds of “fallen angels” – former investment grade companies that had been downgraded below investment grade. Investment banks, led by Drexel Burnham Lambert, launched the modern high yield market in the 1980s by selling new bonds from companies with below-investment grade ratings, mainly to finance mergers and acquisitions or leveraged buyouts.

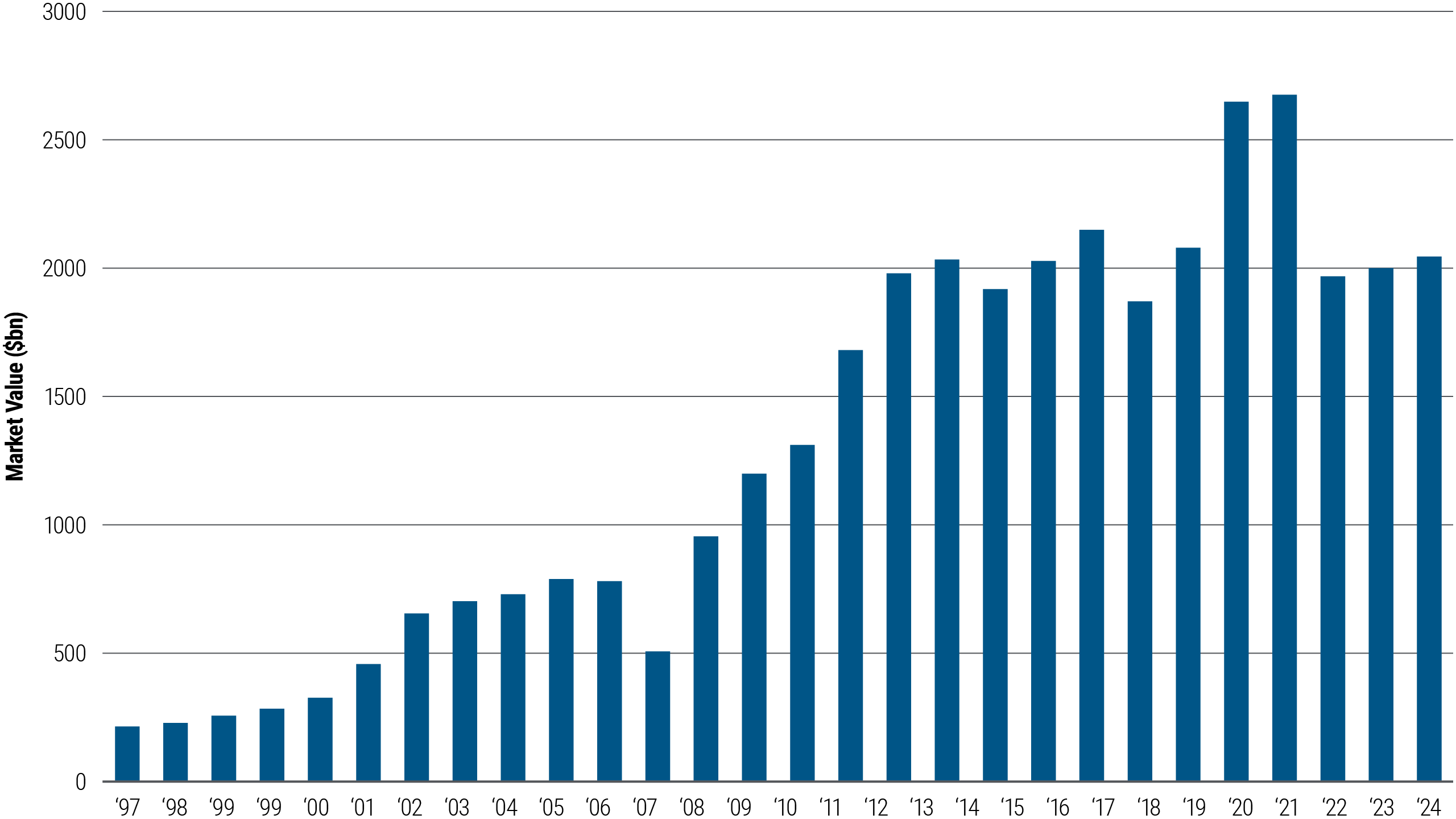

The high yield market has since evolved, and today, much high yield debt is used for general corporate purposes, such as financing capital needs or consolidating and paying down bank lines of credit. Mainly focused in the U.S. through the 1980s and 1990s, the high yield sector has since grown significantly around the globe in terms of issuance, outstanding securities, and investor interest. The chart below shows the growth of the high yield bond market with 2024 data reported year to date.

Growth of Global High Yield Bond Market

Source: ICE as of 31 July 2024

New high yield issuance can vary greatly from year to year depending on economic and market conditions, typically expanding along with economic growth, when investors’ appetite for risk often increases, and waning in recessions or market environments, when investors are more cautious.

The high yield sector includes both originally issued high yield bonds and the outstanding bonds of fallen angels, which can have a significant impact on the overall size of the market if large or numerous companies are downgraded to high yield status. Conversely, the sector can shrink when companies are upgraded out of the speculative grade market into the investment grade sector.

Why invest in high yield bonds?

High yield bonds may offer investors a number of potential benefits, coupled with specific risks. Investors can endeavor to manage the risks in high yield bonds by diversifying their holdings across issuers, industries, and regions, and by carefully monitoring each issuer’s financial health. Below are the key potential benefits of investing in high yield bonds.

- Diversification: High yield bonds typically have a low correlation to investment grade fixed income sectors, such as Treasuries and highly rated corporate debt, which means that adding high yield securities to a broad fixed income portfolio may enhance portfolio diversification. Diversification does not insure against loss, but it can help decrease overall portfolio risk and improve the consistency of returns.

- Enhanced current income: To encourage investment, high yield bonds usually offer significantly greater yields than government bonds and many investment grade corporate bonds. Average yields in the sector vary depending on the economic climate, generally rising during downturns when default risk also rises (high yield companies may be more negatively affected by adverse market conditions than investment grade companies).

- Capital appreciation: An economic upturn or improved performance at the issuing company can have a significant impact on the price of a high yield bond. This capital appreciation is an important component of a total return investment approach. Events that can push up the price of a bond include ratings upgrades, improved earnings reports, mergers and acquisitions, management changes, positive product developments or market-related events. Of course, if an issuer’s financial health deteriorates, rating agencies may downgrade the bonds, which can reduce their value.

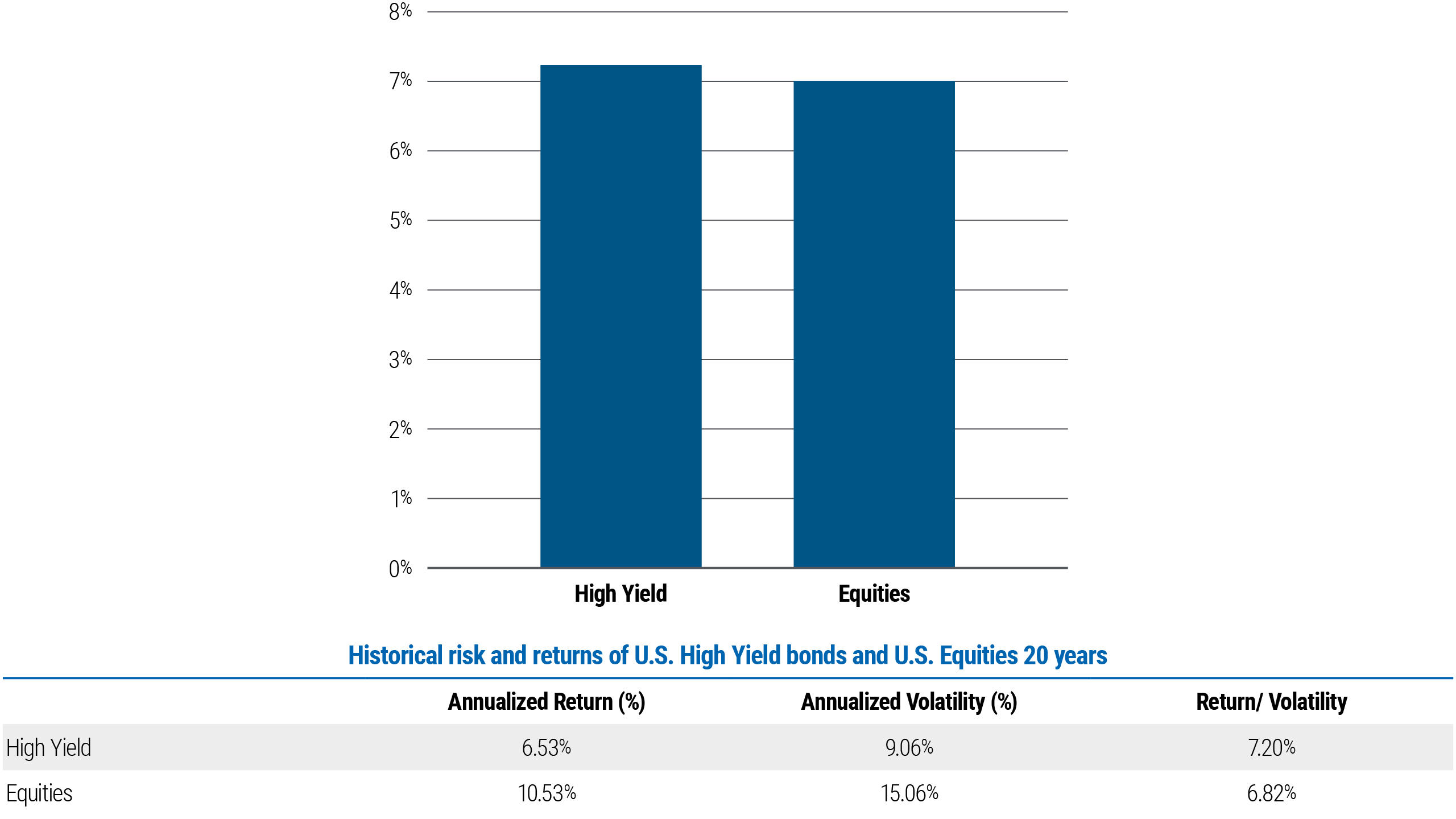

- Equity-like, long-term return potential: High yield bonds and equities tend to respond in a similar way to the overall market environment, which can lead to similar return profiles over a full market cycle. However, returns on high yield bonds tend to be less volatile because the income component of the return is typically larger, providing an added measure of stability. In addition, the combination of enhanced yield and the potential for capital appreciation (though less than for equities) means that high yield bonds can offer equity-like total returns over the long term. Also, bondholders have priority over stockholders in a company’s capital structure in the event of bankruptcy or liquidation; high yield bond investors therefore have a greater chance of recovering their investment than equity investors.

- Relatively low duration: One reason high yield bonds often have relatively low duration is that they tend to have shorter maturities; they are typically issued with terms of 10 years or less and are often callable after four or five years. Generally, high yield bond prices are much more sensitive to the economic outlook and corporate earnings than to day-to-day fluctuations in interest rates. In a rising rate environment, as would be expected in the recovery phase of the economic cycle, high yield bonds would be expected to outperform many other fixed income classes. That said, the high yield sector does not demand great economic times; most issuers may function very well and continue to reliably service their debt in a low growth environment.

20-Year Return/Volatility

Source: BofA Merrill Lynch, Bloomberg, PIMCO as of 31 July 2024

High Yield represented by the ICE BofA Merrill Lynch U.S. High Yield Index

Equities represented by the S&P 500 Index

What are the risks?

Compared to investment grade corporate and sovereign bonds, high yield bonds are more volatile with a higher default risk among underlying issuers. In times of economic stress, defaults may spike, making the asset class more sensitive to the economic outlook than other sectors of the bond market. High yield bonds share attributes of both fixed income and equities and can be used as part of a diversified portfolio allocation.